A Congress Without Lobbyists and the Coming End of Federal Reserve Independence

A Congress Without Lobbyists and the Coming End of Federal Reserve Independence

The creation of the small business lending program points the way to a healthier politics.

Hi,

Welcome to BIG, a newsletter about the politics of monopoly. If you’d like to sign up, you can do so here. Or just read on…

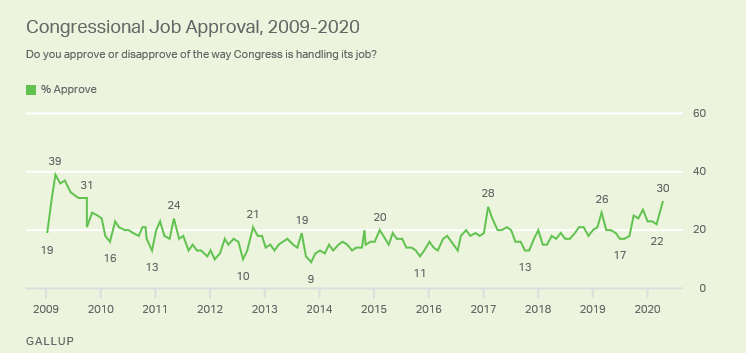

Today I’m going to make a few observations about small business lending, the Fed, and Congress. The pandemic signified a new ideological era, with aggressive state power openly used to structure markets. No one is pretending that our democratic government is a hostile predatory force separate from the people, the debate is over how the government should wield its power. One interesting political dynamic is that the public is starting to like Congress again, with the legislature’s approval rating hitting 30% for the first time since 2009.

I find this a strange result of the pandemic, considering how bad the coronavirus bailout packages were. Nevertheless, I’ve always believed that a good chunk of popular anger at Congress is not dislike of its substantive policy choices, but a frustration that Congress doesn’t seem to do anything. The low popularity of Congress created a toxic dynamic, where members of Congress become afraid to act because voters don’t trust them, and then voters don’t trust them precisely because they don’t act. What this usually meant is Congress would kick decisions to the Fed, or to the military. Now that Congress has acted powerfully, however, voters are responding. And I suspect that an over-powered Fed and what could become a more confident Congress are set up to clash.

I also want to highlight a natural experiment in campaign finance reform, which is that the coronavirus pandemic forced Congress to stop having meetings and fundraisers with lobbyists. The result, I think, was fascinating.

The Federal Reserve vs Small Business

There are so far two basic thrusts through which Congress has acted in the various laws passed in response to the coronavirus. The first is by empowering the Federal Reserve to print money and hand it to Wall Street, and the second is by super-charging the Small Business Administration, a cabinet level department that supervises lending directly to small businesses. The Fed and the SBA are institutional opposites; the Fed seeks to act through New York capital markets, while the SBA is designed to bypass them.

Here are four observations about this dynamic.

(1) The Small Business Lending Program Works

The most significant government action to support business outside the Fed is the Paycheck Protection Program, a $349 billion loan/grant SBA facility designed to help small businesses meet payroll. Media coverage often focuses on program abuse, such as that highlighted by restaurant chain Ruth Chris taking out $20 million through a legal shell game, as well as general frustration getting access to government loans.

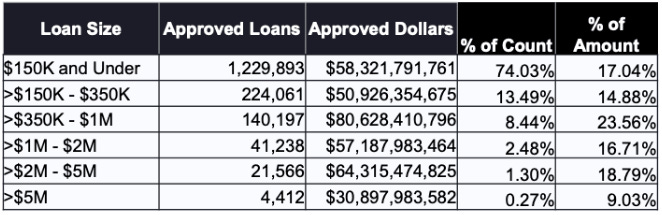

The problems are real, and serious. No doubt there will likely be a lot of fraud, like executives putting their family members on payroll as fake employees. And private equity is aggressive in trying to get their hands on this pot of money, so far largely unsuccessfully. But what Congress and the SBA did is simply remarkable. Within just a few weeks, they got $342B out the door to over 1.67 million businesses, with a vast majority of the loans going to businesses who took less than $150,000 in borrowing.

To offer some perspective, there are 8 million establishments who actually employ someone in America, which means that one in five businesses with an employee in America has gotten a loan from this program. (There are roughly 30 million small businesses in America, though many of those are simply people who are self-employed.) The program will be reauthorized and expanded, so even more businesses are going to get funding. Moreover, the program is largely working through community and small banks, as big banks, despite claims to economies of scale, are in reality giant inept bureaucracies.

The program is also, tacitly at least, both an anti-monopoly program and a private equity reform program. Small businesses that stay alive can challenge the giants, so that’s the anti-monopoly aspect. In terms of private equity, as the Wall Street Journal reported, some private equity owned portfolio companies are going so far as to change their corporate charters so they can get access to the money. In other words, private equity financiers are having to loosen their grip on their assets. For all the screeching about attaching strings to bailout money, the only program with any guardrails at all is the small business lending program.

(2) Congress Can Legislate Without Lobbyists

So how did this program come together? Readers of BIG would have been early in understanding policymaking around small business, because I wrote up in early March how Marco Rubio was focused on moving small business lending as a response to the crisis. Soon after he did so, Congress physically closed itself off to visitors coming in for meetings, and they ended up not holding physical fundraisers anymore.

A lot of people only see Congress as an abstract entity, but Congress is also a physical place, and that physicality matters. Lobbyists have power in many ways simply because they are physically around, and politicians don’t like to say no. During the pandemic, members couldn’t meet with lobbyists, and they couldn’t physically take campaign finance money at fundraisers (which is where a lot of policy talk happens). So they didn’t have to say no to anyone in person, because no one was around to ask them for stuff.

As negotiations over the giant Coronavirus package moved forward, Mitch McConnell deputized Senator Marco Rubio, who was the Chair of the Small Business Committee, to come up with an acceptable small business package. He sat in the Small Business Committee room with a laptop, for days, as Senators came and went to offer feedback and ideas.

Rubio had as a loose working group Susan Collins, Ben Cardin, and Jeanne Shaheen, two Republicans and two Democrats, who over time defined the Paycheck Protection Program. There were no lobbyists in the room, and the Senators were themselves negotiating with each other directly. They didn’t have an endless surfeit of meetings, but could take the time to make policy. The result was a program largely designed to get money out quickly, with consensus from all major stakeholders.

Moving forward, this gang of Senators is doing oversight, working on fixes, and generally, well, governing. So far, and this may change, private equity has been kept out of the main pots of money. Where Senators actually got together and made policy, they did so with physical distance from monied interests, and without the clatter of meetings and votes and events. (Incidentally, one simple recommendation is that Congress actually establish a day every month where no outside visitors are allowed, so members can just talk to each other.)

None of this is to say that the bailout was a good bill, it was in my view a corporate coup. And even beyond the straight slush funds that we knew about at the time, someone slipped corrupt and expensive tax provisions in the bill, and the Fed got its powers expanded and eroded public disclosure provisions. Moreover, Nancy Pelosi’s choice in response to the crisis was to send all members of the House home, and do all negotiating herself. So the House really has been demobilized. But it is interesting that in the one program area negotiated in a relatively straightforward manner, and done through the democratic areas of government versus the secretive Fed, the program is functioning reasonably well.

(3) Small Banks Are Competent, Big Banks Are Not

One of the more heated debates in banking politics is the importance of size. Traditionally, reformers have attacked large financial institutions using the label Too Big to Fail, alleging big banks were dangerous because they took on too much risk and could bring down the financial system. A very powerful counter-argument is that as risky as they might be, big banks are necessary. Big banks, so goes the argument, are simply more efficient than small banks because banking is a scale business.

Bank lobbyists love to argue for the benefits of scale, as do their allies at the Federal Reserve. Cleveland Fed Chair Loretta Mester, for instance, in 2010 dismissed research showing small banks are perfectly efficient, and argued that there were “significant scale economies at even the largest banks.” I don’t mean to pick on Mester, it’s a commonly held view that defending small banks is a vestige of nostalgic populists yearning for the days of yore, versus the savvy Jamie Dimon-types who, whatever you might say about risk-taking, are capable of acting.

As it turns out, however it’s the big guys who can’t actually get things done. What we are seeing with the small business lending program is big banks are not only risky, but incompetent. Here’s the LA Times:

Small businesses that rushed in vain to tap $349 billion in emergency U.S. loans to survive the coronavirus crisis are facing a harsh reality: Some of the nation’s top banks lagged behind relatively tiny rivals in handling applications.

As banking giants tried to automate the process, hundreds of employees at Texas lender Cullen/Frost Bankers Inc. volunteered to fill out forms manually, working late into the night in homes to set up $3 billion in loans. That contrasts with Wells Fargo & Co., which arranged only about $120 million by the time the program was depleted this week, according to people briefed on its progress.

A lot of the arguments for the importance of scale in banking boiled to fake commentary about technology spending, and how fancy big banks hired fancy IT specialists to fancy fancy. (I’m paraphrasing.) Of course many of us have been told that big bank IT infrastructure is terrible, often smoke and mirrors, and that in fact big banks have few commercial banking relationships and little ability to lend to ordinary people except through highly automated programs like credit cards.

And not only were smaller banks nimbler and more effective, but it was larger banks that caused some of the corruption problems, like the wildly inappropriate loans to Ruth Chris by J.P. Morgan. I suspect this failure by big banks, and the success of small ones in lending, will have lasting political consequences.

To offer a historical analogy, in the 1933 banking crisis, many cities ran out of cash, and began issuing municipally created scrip backed by future tax collections. Locally owned stores tend to accept this scrip, while national chain stores did not. Popular anger at this anti-social behavior by chains boosted the movement against chain stores, which in the late 1930s had a series of policy victories to reign in the big guys.

I suspect we will see a repeat. It’s one thing to blow up the world economy, which big banks did in 2008. It’s another thing to not be able to actually make loans. I mean, if Wells Fargo can’t make loans when the government gives them a guaranteed return, what’s even the point of Wells Fargo except as an institution for politicians to yell at when caught yet again for opening up fake customer accounts?

(4) The Federal Reserve Is an Enemy of Small Banks and Small Business

One of the most important trends in banking over the last four decades is the collapse of small banks. As Barrons reported, “In 1985, there were 18,033 FDIC-insured banks across the U.S.; by 2018, there were just 5,477 such banks across the U.S. This has not only resulted in fewer banks, but larger banks.” Why is this? One of the big reasons is that it’s hard to get a new bank charter, because regulators don’t want new banks for fear they will fail. But another reason is that the Federal Reserve and DOJ simply have not used their shared antitrust authority to block mergers. From 1989-1994, there were 4000 merger applications for bank mergers, and the Department of Justice did not block a single one (though it did force some branch divestitures). And the Fed did not formally deny a single merger from 2006-2017. That record is… bad.

This hostility to small banks is continuing in the way the Fed is administering its programs. Take the way that the Fed is handing out favors to big banks and big business versus charging money to small banks for doing small business loans. One of the key programs is the Fed buying various corporate bonds, and when the Fed announced this program the prices of these bonds all shot up. The Fed will likely be buying these bonds at a mark-up, or at the very least at the elevated market price. Yet the Fed won’t even buy the government-guaranteed small business loans from banks, instead lending against them at a cost of 35 basis points. To put it differently, if you’re big you get a subsidy, if you’re small you get a fee.

What Does This Mean?

In early March, I noted that Congress was taking the lead in governing, and then a few weeks ago described how the leaders here are from the populist right, and how they are focused on small business. As it turns out, Congress, when forced to take responsibility, does a very good job, because democracy works.

There is a latent political competition between Wall Street, backed by the Fed, and everyone else in business, who are whether they know it or not, backed by Congress. And for the last forty years, the Fed has been winning, such that the Fed’s power is outrageous; the central bank now conducts everything from major rescue operations all over the economy to its own foreign policy vis-a-vis who gets access to dollars.

Finally, however, there’s an institutional challenge. It’s appropriate that Congress and the Small Business Administration is a focal point for this challenge, because the SBA is the descendent of the Reconstruction Finance Corporation, which was the competitor to the Fed in the 1930s. The SBA was created by none other than Congressman Wright Patman, who was a major character in my book on monopoly power. The animating battles of his life were those against the Federal Reserve and corporate monopolies. In this crisis, we can see why it’s the same fight.

I’m not optimistic about where we are, because the bailout packages were tilted too heavily to the powerful. But there is an outline for a different path, if policymakers choose it.

What I’m Reading

As Amazon Rises, So Does the Opposition, NYT. This is a great profile of Stacy Mitchell of the Institute for Local Self-Reliance. Mitchell is one of the most important political thinkers in the country, advocating for the interests of small business and connecting that fight with broader democratic aims. Also, one of the books on her shelf is Goliath. Flattery will get you everywhere.

A Beer Shortage?, MovieWeb. There’s a shortage of carbon dioxide production, so carbonated beverage producers and brewers are beginning to prepare for a lack of carbonation. What’s happening is that carbon dioxide is largely a byproduct of ethanol, and the collapse of oil prices means that North American producers have shut 34 of 45 ethanol plants. “Everything is so interconnected,” said CEO of the Compressed Gas Association Rich Gottwald. One unnoticed angle here is industry consolidation. In 2016, Air Liquide bought Airgas, and in 2018, industrial gas giants Linde and Praxair merged, selling off some carbon dioxide production to a private equity fund. I don’t know whether this consolidation had any impact on the current shortage, though Praxair was raising CO2 prices before the pandemic and monopolies to tend to cut capacity.

Neiman Marcus to File for Bankruptcy as Soon as This Week-Sources, NYT. Neiman Marcus joins fellow deadbeat junk bond issuers Frontier Communications Corp, LSC Communications Inc, and Quorum Health Corp, who have defaulted on $14.3 billion in April. Bank of America predicts junk bond defaults at 20% in the next two years, while Goldman pegs the number at 13% by year end. Meanwhile, Moody’s and S&P have lowered the bond ratings of cheerleading monopoly Varsity Brands to junk status.

Facebook and Google to be forced to share advertising revenue with Australian media companies, The Guardian. I’m gathering thoughts on what this proposal means. I’m skeptical, but the crisis of the press has accelerated with the pandemic.

Congress Is Investigating Whether a Ventilator Company Is Gouging the U.S. — and Why the Government Is Letting It Happen, GovExec. This piece is all about a loophole I’ve written about in government contracting, the commercial item exception.

The 737 MAX Has Been Grounded for a Year Because of Its Terrible Computers, Popular Mechanics. The Boeing bailout might happen, but reorganizing a capital structure can only take you so far. If the planes don’t work, they don’t work.

Thanks for reading. And if you liked this essay, you can sign up here for more issues of BIG, a newsletter on how to restore fair commerce, innovation and democracy. If you want to a book to hunker down with while sheltering in place, read my book, Goliath: The 100-Year War Between Monopoly Power and Democracy.

cheers,

Matt Stoller

P.S. I got a lot of new readers in the private equity world over the last few weeks. Welcome. I have a question for those of you who are in that industry, or in the credit markets. Are you seeing signs of looming defaults out there aside from the ones I mentioned? I don’t have a Bloomberg terminal and I’m not a trader, so that world is opaque to me.

a more upbeat article than some of the previous i’ve read. i’ve been saying for years, that nothing was going to change for the better until we, collectively, could see the bottom. maybe, as an unintended consequence of the bungled pandemic we’re actually seeing this coke to fruition?

there are now, for the first time, glimpses of seeing a positive change due to a collective reconciliation through this process. it’s become apparent that no matter where you sit, to the left or to the right, that we all have the same concerns and want mostly the same things.

maybe, for the first time we can agree that we have a lot more similarities and a lot less differences, and we, united, actually have some power behind our voices in shaping policy that benefits the people.

for every article I read meant to sow discord and division, seeing actual positive changes happening is bringing hope. we need to step up to stop the petty bickering and hold our legislators feet the the fire and start to actually represent us.

either that, or it’s ceding even more control to the actual people making policy and marching towards the promised dystopian future.

how has jeff bezos add $24B to his net worth while tens of millions of americans have completely lost their means?

The lovely fu to indies. Mark Cuban spotted that and called it out. How about you?