An Economy of Overfed Middlemen

An Economy of Overfed Middlemen

A venture capitalist called Equal Ventures just says it straight-up, we seek to invest in monopolization.

Welcome to BIG, a newsletter on the politics of monopoly power. If you’d like to sign up to receive issues over email, you can do so here.

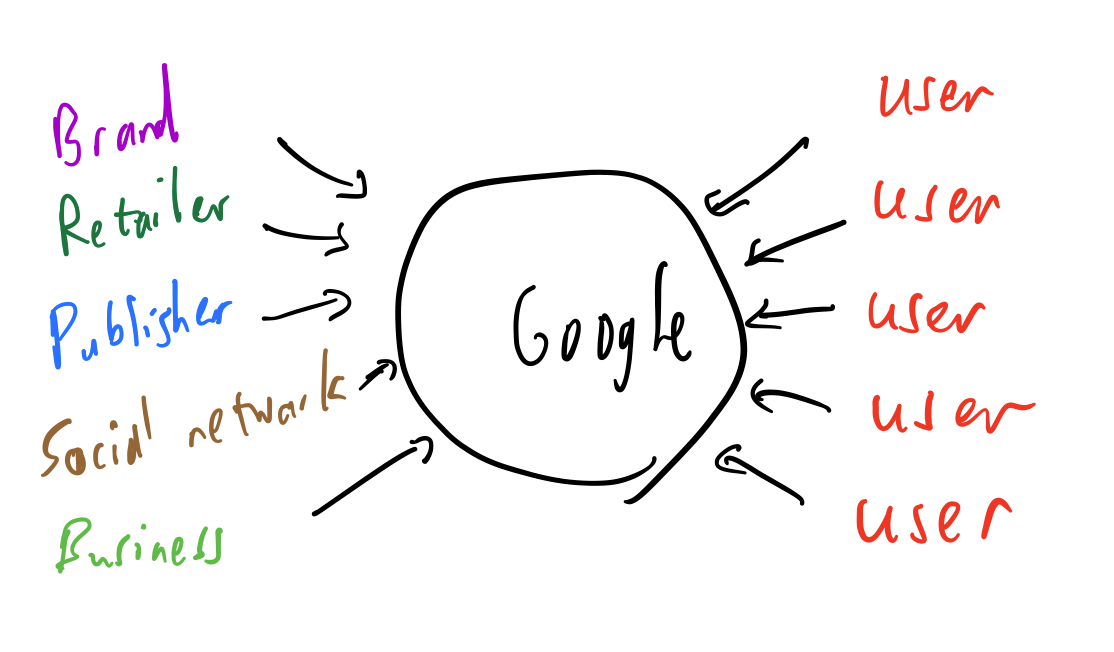

One central problem in our commerce is the outsized role of middlemen. Amazon, Walmart, Vizient, CVS, Google - these are monopolists, yes, but their specific mechanism for exerting monopoly power isn’t controlling production of some item, but in putting themselves in the middle of transactions and taxing one or both sides. Here’s a poorly drawn example of how Google’s search business operates, which will hopefully illustrate the problem.

Whether a user searches for Nike or news about an earthquake, Google is sitting there, matching the user with content. And the search giant imposes a tax for doing the matching in the form of a set of targeted advertisements, which you can see most clearly in the need for firms to buy Google search ads for their own trademarks.

The size of this fee is determined by two factors. The first is the ability and willingness of businesses to pay to access users, essentially their marketing budgets. The second is the ability and willingness of marketing channels to sell access to their users. Normally, if there were a lot of marketing channels and a lot of buyers, the price would adjust and let both groups profit. But Google, because of its market power, has the ability to offer exclusive access to users. Google has roughly 90% of search market share.

Now, one might say that search advertising is only one channel, and surely there are other ways to get customers. And there’s some truth to that, but not as much as one might assume. A few years ago, Amazon did an experiment in Mexico, seeking to see what would happen if it stopped advertising on Google search. Amazon bought paid media on every other available channel from billboards to TV, but its traffic suffered. Google is a monopoly so powerful that it can extract from Amazon, which has perhaps the strongest retail brand name in the world. And that means Google can set the price for firms that need to engage in marketing, which is to say, every firm.

Google uses a host of tactics to exclude others from dislodging or competing with its search engine. Some of these tactics are good, such as creating and maintaining a high quality search engine. But others are predatory, like ensuring that only Google can crawl the web, or forcing the pre-installation of its own apps on user phones to the exclusion of others via contract and payment. Then Google effectively sells access to its users through targeted and search advertising.

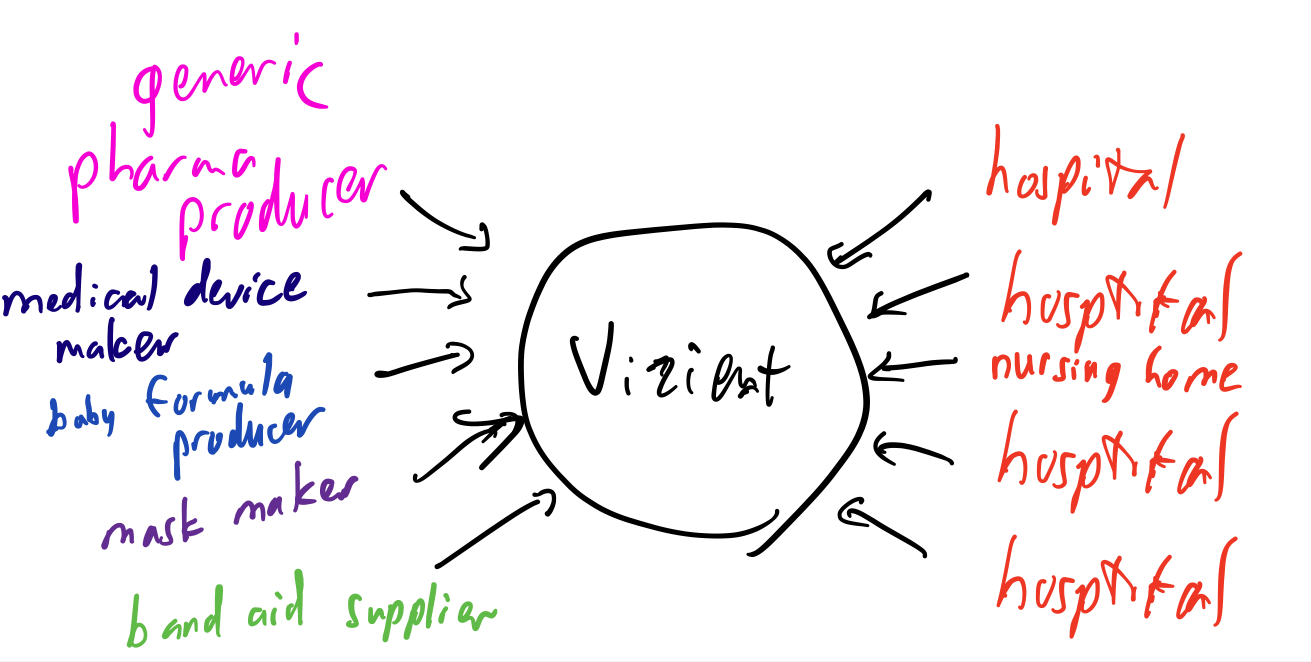

Google is a well-known example, but the middleman model is pervasive. In the $300 billion+ hospital supply market, group purchasing organizations like Vizient place themselves in between health care providers (hospitals, nursing homes, etc) and suppliers of health care providers. And then they impose taxes on the marketplace they control. Here’s another badly drawn illustration of one of the dominant GPOs, Vizient, and how it operates.

After a bevy of mergers, there are now three major GPOs, and they use similar tactics as Google, like rebating arrangements with hospitals to concentrate buying power. Then on the supply side, everyone from pharmaceutical or medical device producers to band aid and baby formula suppliers have to pay GPOs to get access to the hospital market. The ability of GPOs to extract fees and control markets has led to serious shortages in health care supplies, and raised costs dramatically. But it’s just another variant of how middlemen operate in general.

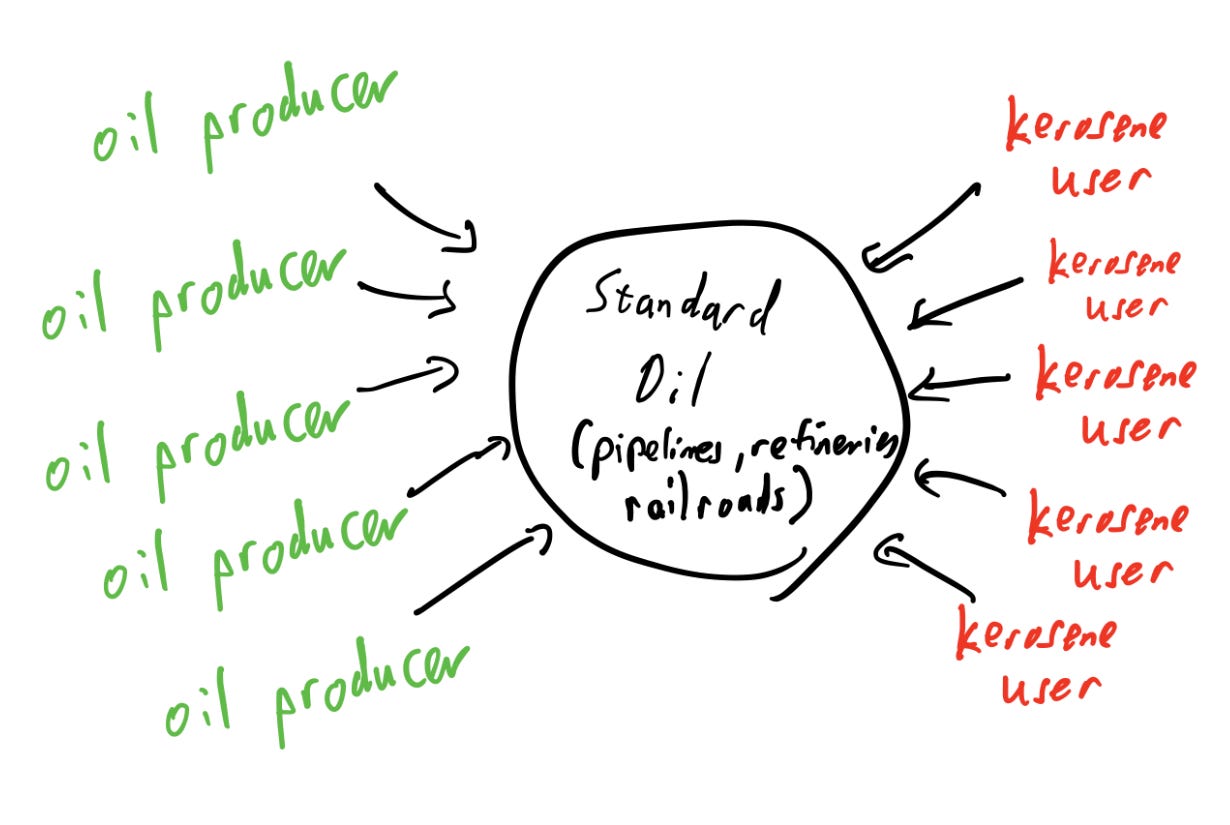

I could do badly drawn examples of many monopolies who use this basic model. Here’s the granddaddy of monopoly power, Standard Oil, which monopolized refining and controlled railroads and pipelines in order to impose a tax on oil producers and kerosene users.

In this case, oil producers were very much in the position of medical suppliers selling to hospitals through GPOs, or content producers trying to get to users through Google. A bevy of laws, like the Sherman Act, the Clayton Act, and the Robinson-Patman Act, were passed to block the exploitation of dominant middlemen. And such law should be usable today against firms like Google, since Google, while technologically different than Standard Oil, is fundamentally using similar tactics. But antitrust laws have gone largely unenforced for four decades.

Today, this middleman model is so pervasive that venture capitalists are now promoting investment models based on explicit violation of antitrust laws. Take a seed fund called Equal Ventures, launched a few years ago with a specific thesis of looking for middlemen monopolist. In a Medium post, one of the founders noted that his venture invests in monopolization, which, though it feels quaint to say this, is literally outlawed by the Sherman Antitrust Act. I’ve bolded the relevant parts because it’s just so stark.

A big part of our belief in transforming legacy markets is understanding the economics of those industries and determining the opportunity for the company to carve out a “moat” in that industry’s value chain. While companies never have a moat on Day One, we try to evaluate their “moat trajectory”, which is the long-term sustainable advantage they can have over competitors IF everything goes according to plan. Generally this means the company has the ability to monopolize a segment of the value chain and sustain it given a flywheel inherent in their business model.

Generally speaking, we want to see the ability to monopolize a $1b+ segment of a total addressable market (margin, not revenue). We can get comfortable with smaller TAM segments provided that 1) there is a near-term path to achieving that (will discuss this shortly) and 2) we believe the segment lends itself well to monopolization, rather than many players.

Ultimately, we want companies capable of generating long term FCF, and that requires a defensible moat position in the market, not a leaky bucket with lots of revenue.

The text of the Sherman Act bars ‘monopolization,’ so to write that one is trying to build firms that can ‘monopolize’ is, well, remarkable. Equal Ventures organizes its investments by putting money into what it thinks will be middlemen monopolies, like an AirBNB for child care or an eBay for excess inventory. These are reasonable business ideas, but the goal here isn’t merely to deliver some useful matching service and make money, but to ensure dominance. Such investment strategies end up pushing risk or production off to others, while seizing control of a key link in a supply chain. That’s not just my view, it is literally what the investors say they are doing when they state they want investments where the “company has the ability to monopolize a segment of the value chain.”

Our economy is so pervasively threatened by middlemen that there are even middlemen of middlemen, such as Amazon third party seller roll-up Thrasios, which Equal Ventures admires. Thrasios has bought thousands of third party sellers on Amazon, and is able to use its bulk to negotiate better terms from Amazon. As my colleague Krista Brown detailed, there’s very little real value here, just predation and mergers in a monopoly ecosystem. Amazon is such a big middleman that it can effectively outsource some predation to a smaller middleman.

Increasingly, policymakers and scholars are recognizing this middleman problem. The FTC has started to revive the Robinson-Patman Act, a law that prohibits the use of rebates by middlemen to control markets. And in her new book Direct, anti-monopoly scholar Kate Judge describes how a monopolized middleman economic order works, and what it is doing to our democracy. It’s not that middlemen are per se bad, the role of matching suppliers and buyers is useful. The problem is when middlemen turn into monopolies. Consolidated middlemen keep a swollen amount of the transaction amounts they mediate. And by manipulating pricing, middlemen can break markets and turn investment towards unproductive uses.

One core problem we have with our economy is that our business people are focused on controlling what others produce, instead of producing themselves. If we simply got rid of the legal arrangements fostering this business model, then we would have a very different set of commercial arrangements.

All companies are looking for their moat.. some edge that creates a barrier to entry that reduces threats of competition. The only thing is not all moats are the same, and how they are judged and regulated probably shouldn't be the same.

Its one thing for a company to build moats through anti-competitive behavior (mergers, predatory pricing). Its another if a company is able to build a moat through innovation, where the market gravitates to their new product because it just adds so much value. There are also businesses where their viability depends on a critical mass of users (social network, online exchange, trading platform), which in itself is a significant moat.

The latter two examples I think are situations where there are net benefits to society in moat-creating. But the former, obviously not. There's probably a decent grey line in between which I think is the trickiest to judge, but deserves public scrutiny.

Thrasio is literally every Consumer Package Goods (CPG) platform but just selling on Amazon instead of big box retailers.

Connecting buyers with sellers is actually hard. Which is why you’re writing on Substack and not some random Wordpress blog.