Antitrust Guidelines and Overthrowing a Corrupt Priesthood

Antitrust Guidelines and Overthrowing a Corrupt Priesthood

A year ago, the antitrust agencies got thousands of comments from us. And now they are telling us how they are acting. This is the nerdy stuff that matters, and you can participate.

Welcome to BIG, a newsletter on the politics of monopoly power. If you’d like to sign up to receive issues over email, you can do so here.

Today’s issue is about an obscure but important document on corporate power released this week known as merger guidelines. It is in many ways the overthrow of the corrupt antitrust priesthood.

If you already know what these are and want to help, then tell the government what you think about mergers and antitrust by submitting a comment here. If you need more information, read on. Because this particular issue of BIG is important. There aren’t a lot of real actions people can take to influence government, but this one is real, and will make a meaningful difference in whether we truly address corporate power.

In 1517, a German priest named Martin Luther launched one of the most significant social movements in history by posting a document known as the Ninety-five Theses on the door of All Saints' Church in Wittenberg. It became known as the Protestant Reformation, and was an argument that the Catholic Church, the most potent religious and political force in Europe, had been taken over by a corrupt priesthood more interested in making money than saving souls.

In particular, Luther attacked the sale of indulgences, which were certificates sold to the wealthy and powerful to reduce the amount of painful time spent in purgatory in the afterlife. There had been heretics before, but they had mostly failed. The Catholic Church had typically responded to reformers by dismissing all concerns from less sophisticated local people. Only priests spoke Latin and had access to bibles, which were transcribed carefully one by one in monasteries.

This time, however, Luther’s argument found deep resonance. With the creation of the moveable type printing press in the 1440s, and the spread of this technology, the bible was soon mass produced and sold all over Europe. Luther’s reformation happened when a bunch of “lay” outsiders professed to be able to read the bible for themselves in their vernacular, and determined the true religious meaning for themselves. It was a battle of text and common understanding versus supposedly authority. Luther went after a corrupt priesthood making money from practices based on ideas that just weren’t in the religious texts they were supposed to be interpreting. When more people read those texts, they realized Luther was right.

Over the past four days, I’ve been watching the business press go crazy about an obscure document that the antitrust agencies put out, known as ‘merger guidelines.’ And like the Catholic Church of the 1500s, or really members of any authoritarian social hierarchy, the antitrust priesthood is very upset.

For instance, Larry Summers, the avatar of Democratic Party economic policymaking under both Bill Clinton and Barack Obama, is in a rage, asserting these represent a “war on business.” Biglaw firms are sending out alerts to clients, saying “investors, boards and C-suites should anticipate significant delays and expenses associated with a far broader range of proposed transactions.” And the House Republicans are even trying to defund the very ability of the government to publish this document in their government funding bills.

Why does this document create such anger? The answer is that it is an attempt to return antitrust back to the rule of law, and away from the corporate revolution of the 1980s. And Wall Street and the Antitrust Bar - replete with a pope - simply cannot believe that anyone would dare interfere with their consolidating ways. They are, in a sense, the Catholic Church, having sold indulgences for so long that they will not accept that such a practice has no basis in the underlying text they interpret. And we, the ordinary people given access to the case law, history and statutes by the internet, realize their authority is based on a lie.

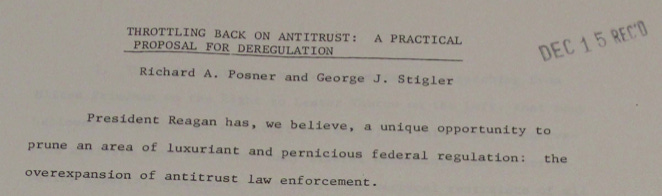

A year and a half ago, I wrote a piece titled “The Secret Plot to Unleash Corporate Power.” In it I described a scheme by Chicago School scholars in 1982 to administratively rewrite antitrust law without going through Congress. At the time, Reagan officials knew they couldn’t get Congress to change the statutes, because Americans dislike monopolies and support strong antitrust enforcement. So they pursued a strategy, and evidence of this came from documents in the Reagan library, to simply not enforce antitrust laws.

Richard Posner and George Stigler, both legendary Chicago Schoolers, penned this transition memo describing their scheme.

Their main recommendation was that Reagan appoint antitrust leaders who would change enforcement priorities by issuing different merger guidelines, which was the way the Department of Justice instructed courts and business leaders as to what was and wasn’t legal. In 1982, Bill Baxter, who was Reagan’s Antitrust Division chief, did so. Decades later, antitrust officials would analogize these merger guidelines to legendary jazz albums that changed music forever. And the metaphor wasn’t wrong.

The impact of this new non-enforcement mandate had large and immediate effects on our society. The red arrow is the moment that the Reagan administration issued their merger guideline rewrite.

Merger mania started instantly, in everything from retail to defense to banking. Indeed, mergers and acquisitions became so important that they came into the culture in a big way, becoming the the basis of the popular 1987 movie Wall Street, which coined the memorable phrase ‘Greed is good' that characterized the 1980s. Bill Clinton, George W. Bush, Barack Obama, and Donald Trump all continued the framework Baxter laid out, and over the next forty years there were successive merger waves to consolidate nearly every nook and cranny of American commerce.

It’s hard to find a part of America that has remained unaffected, with much higher prices on vital medicines, low-priced medicine in shortage, reduced wages, and massively irritated Taylor Swift fans. Today Hollywood is aflame because the industry itself is collapsing, with the quality of movies dropping because of the huge roll-up of power by a few giant studios. The internet is a wasteland, newspapers are disappearing due to online ad monopolies, and the defense industry can’t make enough ammunition because all black powder production consolidated into one Louisiana factory, which blew up.

Mergers Ruin Everything

Nearly every major dangerous social trend today, from wage inequality to regional collapse to social despair to the inability to efficiently shift energy sources, is a result of monopolization, and mergers are the primary mechanism through which firms monopolize. In 1890, 1913, 1950, and 1975, Congress passed various laws to deal with it. The current key law on mergers today is called the Clayton Act, and it is still on the books. Unfortunately, because of the Reagan administration, and the ideological acceptance by the Democrats of what Reagan wrought, under-enforcement has been so poor that, well, Ticketmaster.

In 2008, this crisis came to a head with the collapse of banks, bringing home that Too Big to Fail is a serious social problem. Using the internet and journalism, a new wave of reformers began to argue that the Chicago School philosophy was hopelessly naive and reckless, and not tethered to any form of law or Congressional mandate. It was wholly made up by a corrupt priesthood.

This group of reformers has made a lot of progress. Since the end of the Obama administration, there were halting efforts to restore enforcement, especially with mergers where a company is trying to roll up an entire industry by acquiring everyone in it to build walled gardens of power. (The attempt to turn movies/TV into a walled garden is what’s destroying Hollywood right now.) Trump’s attempt to block AT&T-Time Warner signaled a shift, and his 2020 monopolization suit against Google showed the turn was real.

Today, the Biden administration is aggressively enforcing antitrust laws. There’s an argument from the corrupt priesthood that this is a failed strategy, but it’s actually working quite well. Indeed, the Federal Trade Commission has won nearly all of the challenges they have brought, from mergers in sports retailing, cement, and pipelines to a monopolization claim against Surescripts. But a few high profile losses, such as Meta-Within and Microsoft-Activision, do indicate that the priesthood still has power within the judiciary.

And that brings us back to the merger guidelines. These guidelines help instruct the courts how to interpret a complicated area of law. One problem is that successive versions of merger guidelines since 1982 have told judges that most mergers are good. I’m not kidding, or exaggerating. Here’s a sentence from the most recent version of these guidelines, written in 2010: “A primary benefit of mergers to the economy is their potential to generate significant efficiencies and thus enhance the merged firm’s ability and incentive to compete, which may result in lower prices, improved quality, enhanced service, or new products.”

That’s… the opposite of the Clayton Act. The 2010 guidelines, like those written in 1982, basically said that large mergers where rivals bought one another were illegal, but everything else was fine. What’s also astonishing is that these guidelines cited no legal precedent, but were merely guesses from economists using unwieldy and speculative tools. It was a priesthood selling indulgences, with no basis in the underlying text.

Keep in mind, the 2010 guidelines weren’t some right-wing conspiracy, but were written by Obama enforcers, led by economist Carl Shapiro. And this kind of guidance matters. In 2018, Judge Richard Leon ruled in favor of the AT&T-Time Warner merger, citing the guidelines. Shapiro was the expert economist for the government, and while he opposed the merger, he also testified that the merger would save consumers money. It’s no wonder antitrust enforcers lose cases when they tell courts that mergers are good in their own guidance documents and testimony!

Another loss happened last week, when Judge Jacqueline Corley, a Biden appointee, allowed Microsoft to buy Activision in the largest tech merger in history. She decided that, despite evidence Microsoft is seeking to acquire market power, such a merger is good for consumers. It was a blow, and though the Biden enforcers are going to keep bringing cases, and Wall Street isn’t going to launch another merger boom, the case law needs to change. So having the Antitrust Division and the Federal Trade Commission update their guidance to tether it to *actual law* and how markets work is an important step forward.

What Do these Guidelines Say?

Ok, so what do these new draft guidelines say? They present 13 principles, each one tethered to specific legal precedent, on how mergers may violate the law. Some principles are well-understood, like the presumption against big mergers that increase concentration. Others are new, but extend such arguments to labor markets and how workers are affected by mergers. Still others are attempts to update guidance for how the economy has changed, with the rise of institutions like tech platforms and private equity firms.

For instance, one new principle is that the antitrust agencies should look not just at one merger, but at a whole series of mergers, the so-called ‘serial acquisition’ problem. Such roll-ups, where a firm or private equity fund buys a whole slew of small companies in one industry, is common today in the economy, from dental clinics to portable toilets to the income verification service of Equifax. The guidelines indicate that the whole suite of mergers are fair game, not just one specific merger.

Here’s why this kind of update matters. A few days ago, Bloomberg floated a rumor that Disney CEO Bob Iger is musing on selling Disney to Apple. Most of us would think that such a combination would be highly problematic. But the 2010 guidelines probably instructs courts that such a merger is fine.

These new guidelines offer a way for judges, business leaders, and enforcers to understand the legal problem with such a merger. Such a merger might violate four or five of these principles. For instance, Apple is a potential competitor in a number of areas with Disney. It could compete with Disney in movie theaters, as it already produces and distributes films through streaming. That violates principle four, that combinations “should not eliminate a potential entrant in a concentrated market.” It also violates principle seven, that “mergers should not entrench or extend a dominant position,” or number five, which prohibitions “creating a firm that controls products or services that its rivals may use to compete.” Apple, and even Disney, are multi-sided platforms, which has its own principle involving the special way that such tech firms compete.

The entrenchment principle is particularly important in a world of platforms and walled gardens. To explain this one, the agencies cited a 1967 merger case, Proctor & Gamble buying Clorox. P&G was dominant in household products, Clorox in bleach. The combination would have solidified P&G in both markets. As the court wrote, “few firms would have the temerity to challenge a firm as solidly entrenched” as Clorox. Laying out a basic set of principles helps Disney CEO Bob Iger, Apple CEO Tim Cook, as well as judges, understand the problem with combining two immensely powerful firms. The goal of such a merger would be to further entrench Apple’s ecosystem, which locks in consumers.

If these guidelines had been in place during the Microsoft-Activision trial, would the FTC have won? I don’t know. But it’s fairly clear that the industry is now going to consolidate. As The Economist wrote, "Share prices across the [video game] industry have been rising since the ruling, possibly in anticipation of a takeover spree." And that would violate principle number eight, which is that mergers “should not further a trend toward concentration.” In multiple cases, as well as Congressional intent, this principle is good law. But Judge Corley chose to follow the corrupt priesthood, possibly because no one had instructed her to understand the law differently. If this set of guidelines had been in front of her, would the trial have ended differently? Maybe.

How You Can Help

Now, here’s where you come in. Two days ago, I asked a question to Antitrust chief Jonathan Kanter at a Federalist Society event about the role of public comments in this process, and he said that hearing from the public is incredibly important in helping the agencies understand how markets actually work. Thousands of people chimed in a year and a half ago, including doctors, writers, truck drivers, nurses, and software programmers. Now it’s time to do it again. These guidelines are in draft form, they will be finalized soon.

There are 60 days to give our feedback. The government has set up a site on Regulations.gov where you can tell them about your experience with mergers, or offer thoughts on antitrust law, mergers, big business, or unfair methods of business. It looks like this, click on the comment button in the red circle.

So that’s how you can help. Tell the government about your experience with mergers through this site. There are already over one hundred comments, and you can browse and read them. Evan Goldberg, for instance, wrote this.

I work in film and television and am very concerned about the consolidation of power under these big media and tech companies. Writers, producers, directors, actors - we are all feeling the squeeze. They are systemically reducing our power and influence. The WGA/SAG strikes are a cry for help. We need help. Help from the government. This is NOT a problem we can fix on our with picketing and passion. We need policy implemented from the top down that protects us and nurtures business for everyone, not just the corporations at the top. Their predatory tactics are destroying the industry, it's clear as day to anyone. Even people who have nothing to do with entertainment and media seem acutely aware, and it's because at this point most everyone knows someone who has been affected by this shift. The imbalance is significant and the government needs to help.

There are plenty of other comments, on everything from consolidation in health care to groceries. Add your thoughts.

The Pushback

Critics of these new guidelines are making a number of different arguments, but their fundamental claim is that this new document doesn’t reflect the law. What is remarkable about this critique is that the process that Kanter and Khan used to come up with this document was to have the agency staff read every single Supreme Court and appeals court case involving mergers, and then try and characterize what the law actually says.

The process was led by FTC economist Aviv Nevo and DOJ economist Susan Athey, both highly respected mainstream thinkers. To give you a sense of how not-radical these documents are, Athey has won the prestigious John Bates Clark Medal, which is a forerunner to the Nobel Prize in economics. I don’t really care about such baubles, the point is to say that pretty much everyone, except Bork dead-enders, realize that interpretations of antitrust law are out of step with market realities.

Indeed, what’s astonishing is that much of the post-Reagan era gospel on mergers and antitrust is in fact not situated in statute or even case law. It’s purely vibes. Or as Larry Summers put it yesterday, “I think that traditional thinking [on mergers] has had it about right.” Indeed he does think that. And that’s the priesthood we’re overthrowing.

Thanks for reading! Your tips make this newsletter what it is, so please send me tips on weird monopolies, stories I’ve missed, or other thoughts. And if you liked this issue of BIG, you can sign up here for more issues, a newsletter on how to restore fair commerce, innovation and democracy. And consider becoming a paying subscriber to support this work, or if you are a paying subscriber, giving a gift subscription to a friend, colleague, or family member.

cheers,

Matt Stoller

Thanks for the heads up on the new merger guidelines. What a bright ray of hope in the darkness!

Here is the comment I submitted to the FTC:

I am 86 years old, have Bachelors in Physics from Caltech and a PhD in Economics from MIT. I started investing in the market in the 1960s and have followed market trends since then. Increasing numbers and sizes of mergers over time has been highly visible to me. At the same time, as a consumer and interested observer, I began comparing what was happening in industrial and distribution companies over time to what I remembered in the 1950s. By the 1980s, what stood out for me was contrast of worker-management relations then and in the 1950s. I recall that in the 1950s, a common goal of young people was to join a company expecting to work for it, and be cared for by it, for the rest of their lives. And indeed in the 1950s, this mutually beneficial contract was widely honored.

By the 1980s, fueled by junk bonds, Wall Street (short for all financial institutions), began buying up companies that were "not cost efficient," which simply meant that management was not squeezing their employees as much as possible. People who would come into an acquired company and fire people by the thousands, bust unions, and cut the quality of output were highly prized business luminaries. This led to declining quality of life for workers and consumers both. Fixed benefit retirement that was the norm in the 1950s has become nearly as extinct as the dodo -- greatly increasing retirement financial insecurity.

Over time, as more and more consolidation occurred, even though my income rose far fast than measured inflation, I felt less and less satisfied with what I purchased. Airline travel is a prime example. Supermarkets and Walmarts reduced the convenience and variety of buying. Education went from being eminently affordable (I paid under $1000 a year to attend Caltech) to becoming unaffordable except for the rich. Medical care went from the personal and affordable by nearly all to institutional and insanely expensive (I paid over $5000 for a single night's stay in a double room).

I have directly experienced the results of consolidation on the price of papaverine used in surgery and, in my case, to treat erectile dysfunction. When I started using it in about 2000, I paid $10 for 10 ml at a small pharmacy in Mendocino, California. Recently, I was quoted a price of $160 for 10 ml -- a 1600% increase in 23 years! This a generic drug that has around for a long time, no patent protection. But, the big pharmaceutical companies have been able to consolidate the production and distribution of papaverine to the point where it is more like a monopoly than a freely competitive market with many producers and sellers.

One of the most disturbing developments that I only became aware of recently is private equity "rollups" of related small local businesses to create effective monopolies and higher prices.

We are far gone down the path to allowing corporations and banks to become so large that they are "too big to fail" and "too big to regulate."

I heartily support your new merger guidelines. Without a revolution that stops further consolidation, the economic future of the common man will become ever more dismal.

My rule of thumb with Larry Summers is that when he opines on an issue or policy I instinctively take the opposite viewpoint.