How Trump Increased Your Cell Phone Bill

How Trump Increased Your Cell Phone Bill

A set of lawsuits is charging that T-Mobile and Sprint executives lied to the judge who approved their 2020 merger. Now prices are going up. It's time for damages and a break-up.

Welcome to BIG, a newsletter on the politics of monopoly power. If you’d like to sign up to receive issues over email, you can do so here.

Today I’m writing about how the Trump administration, in allowing a merger between T-Mobile and Sprint, ended up causing inflation in cell phone prices. Fortunately, because of some savvy class action lawyers and useful recent precedent, this story may have a happy ending.

Plus, for anti-monopolists in the broader Anglo world, I have a few words on (1) Canadian movie theater monopolist Cineplex and (2) price hikes and market power in the UK.

A Four to Three Merger

Last Friday, the Wall Street Journal’s Drew Fitzgerald wrote a good story about how inflation is driving up the prices that don’t seem related to oil or commodity price spikes, like wireless communication. “Wireless companies have spent the past month boosting fees and raising the cost of some midrange wireless plans,” wrote Fitzgerald. “Industry executives say that consumers already numbed to surging prices for other necessities might absorb slightly higher rates instead of switching providers or dropping service.”

Here are some of the increases.

AT&T raised the cost of its older wireless plan “by up to $6 for single lines and $12 for family plans.”

Verizon raised prices by either $6 or $12 a month on some of its data plans, and slapped a monthly per-smartphone fee of $2.20 on business plans, and raised consumer wireless plans by $1.25 a month.

T-Mobile raised fees on older plans by 31 cents/month, and its activation and support fees by $5.

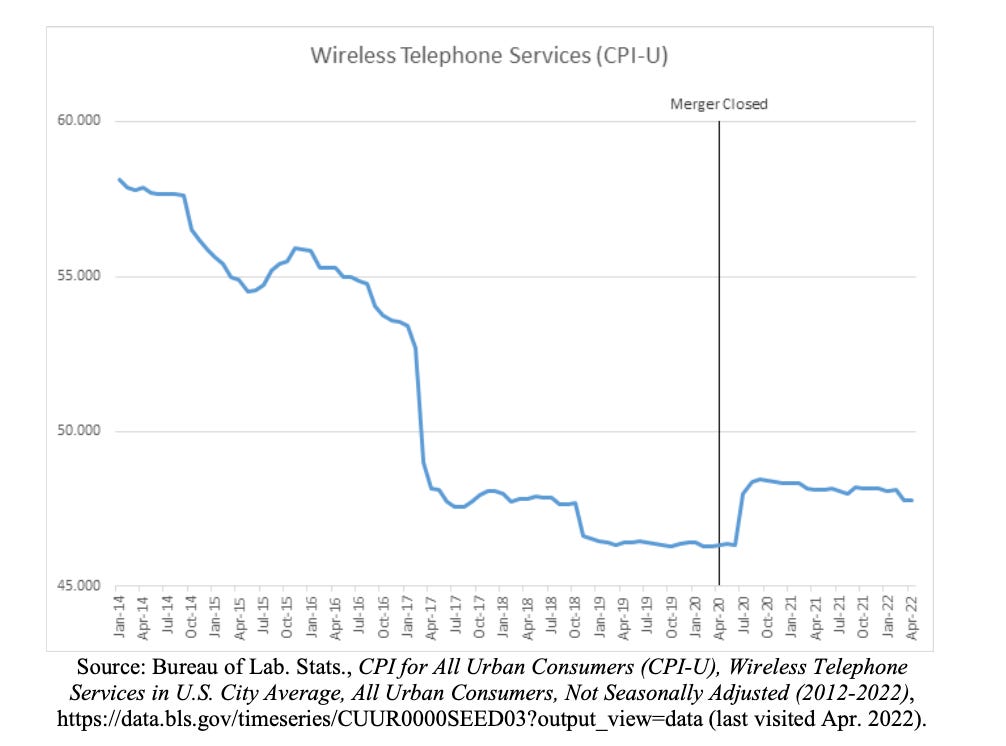

Missing from the story is why these prices are going up. From 2014-2019, cell phone prices had been going down, consistent with what happens in many high tech markets where technology is improving rapidly. There’s no obvious reason for that to have changed. Costs for materials and labor are up a bit, but not enough to substantially dent profit margins in a market largely based on already installed fixed communications equipment. (Plus prices started going up in 2020, before the current bout of broader inflation.) So what happened?

In 2019, there were four major carriers in the market for cell phones. Today, there are just three. And the reason is that the third largest cell phone provider, T-Mobile, was able to buy the fourth biggest, Sprint. In doing so, it ended a price war that had been lowering prices for consumers for six years.

This merger had been a long time coming. For years, T-Mobile, with its magenta clothed CEO John Legere flamboyantly calling itself the ‘Un-carrier,’ had been annoying the industry with its strategy of lowering prices to acquire consumers. It was what is known in economics as a ‘maverick’ firm, pursuing an unusual strategy that forced the whole industry to adapt and become less profitable.

In 2011, AT&T sought to put an end to this maverick strategy by offering to buy T-Mobile. Fortunately, the Obama administration, though generally weak on antitrust, blocked the merger, because antitrust officials, as well as then-FCC Chair Tom Wheeler, believed that a concentrated wireless market with four firms should not be allowed to consolidate further. From 2014 onward, because wireless competition continued, cell phone prices dropped by 6.3% annually.

“Big prizes. So smile and get to the table.”

After AT&T was blocked from buying T-Mobile, and prices dropped, executives across the industry became increasingly agitated about competition in the market. Deutsche Telekom, which owned T-Mobile, saw removing one of four players as essential to cashing out. In 2015, Peter Ewens, T-Mobile’s head of strategy, told CEO Legere that, “if we can’t get four to three consolidation, the industry is headed for commoditization and [Deutsche Telekom] should limit their exposure to the U.S.” Basically, if they couldn’t make a merger happen, they should sell T-Mobile, possibly at a loss.

Enter Donald Trump’s new telecom-friendly administration.

The Obama administration was cozy with big tech but somewhat cold to telecom. By contrast, the Trump administration, with ex-Verizon lawyer Bill Barr as the Attorney General, was deeply aligned with the telecom industry. Immediately after Trump took office, Legere texted the higher-ups at Deutsche Telekom, saying that the “[r]egulatory environment will never be better than now” for a “four-to-three” merger. To highllight this point, he then added, “Big prizes. So smile and get to the table.”

Telecom mergers run through two different agencies, the Federal Communications Commission and the Department of Justice Antitrust Division. Trump chose Verizon lawyer Ajit Pai to run the FCC, and a lobbyist named Makan Delrahim to run point at DOJ. Both approved the merger, with Pai alleging it would be good for the public interest, and Delrahim trying to concoct a silly scheme for DISH to become a fourth major wireless player, (which it had no plans to become and has failed to achieve.)

Multiple states led by Democratic attorneys general tried to step into the breach to stop the merger. It’s difficult for a state to win an antitrust case when the Federal government is telling a judge that there’s no problem. Nonetheless, there was some hope. It was an obviously terrible merger, and the market was working well with four carriers. Unfortunately, a Bill Clinton-appointed judge, Victor Marrero, heard the case, and ruled against the states and for T-Mobile-Sprint. Marrero did so because throughout the process of buying Sprint, T-Mobile executives had promised they would continue its “past pattern of aggressive competition with AT&T and Verizon, and that the merger would therefore not result in higher prices.”

As soon as the merger closed, prices started going up. As DT’s CEO publicly bragged, “It’s harvest time.” It turns out that, yes, Legere had lied to the judge. Shocking, I know.

It was a catastrophic merger for all sorts of reasons. T-Mobile was blocked by the merger agreement from raising its prices directly, but it raised prices in other ways, by hiking fees, changing contractual terms, passing through increases in the cost of third-party benefits like streaming services, and increasing the cost of devices and handsets. T-Mobile refused to let DISH use its network as it had promised, and did not follow through on promises to existing customers.

T-Mobile also immediately started spying on its customers by expanding a surveillance ad business, which is exactly the kind of invasion of privacy as a price hike at the heart of Dina Srinivasan’s theory of Facebook’s monopolization.

But the harm wasn’t isolated to T-Mobile customers. The rest of the industry also raised prices. For instance, in 2021, Verizon had a 4.66% increase in wireless service revenue for consumers, versus 0.4% and 2.5% growth in 2020 and 2019, respectively. AT&T is also raising prices, with its CEO saying on its first quarter call that prices would rise across the telecom industry “over the next several quarters.” T-Mobile also destroyed its independent dealers, shrinking the number of stores and forcing onerous terms on them.

BIG is a reader-supported newsletter focused on the politics of monopoly and finance. This is journalism and advocacy that challenges power, so please consider a paid subscription. You can always get lies for free. The truth costs a few bucks, but in the long run it’s much cheaper.

It was on the face of it one of the most embarrassing mergers that happened under the Trump administration, what I called a ‘jump the shark moment’ for antitrust. Judge Marrero was a credulous moron, buying the story that the combined firms were operating in a complex environment instead of just trying to raise prices. “Milk is milk,” he wrote, comparing cell phones to what he imagines is a simpler product and thus a less “dynamic” market.

But Marrero shouldn’t feel too bad. Other regulators approved the merger as well, and they too had been deceived. For instance, T-Mobile lied to the Public Utilities Commission of California about being willing to deploy capacity to consumers, which it did not. The commission is now looking into the matter. Here, for instance, is the commission accusing T-Mobile of offering bald-face lies about whether the firm would use its spectrum to foster a better customer experience.

The Commission relied on the specific false statements, omissions, and/or misleading assurances T-Mobile gave regarding its use of the PCS spectrum and its repeated references to a three-year customer migration period without a degraded experience in framing D.20-04-008. Further, it appears that these false statements, omissions and/or misleading assurances and the related time references were intended to induce the Commission to approve the merger.

To be fair, some of the promises of the merging party were kept. For instance, Sprint’s Executive Chairman and former CEO Marcelo Claure received an estimated severance payment of $61.5 million, Michel Combes, Sprint’s current CEO, got something like $26.1 million, and Legere himself managed to get more than $137 million out of the deal. All that money, just for lying to one judge. Good work if you can get it.

What Happens When a CEO Lies to a Judge In an Antitrust Suit?

Normally after this kind of disaster, there’s nothing to be done. A CEO lies to a judge, the merger went through, everyone but Wall Street loses, the end. Executives get their perjury bonus.

But that seems to be changing, a bit. In a series of recently filed antitrust suits, plaintiff lawyers are trying to set things right. In one class action complaint on behalf of consumers, a group of premier plaintiff’s law firms filed a lawsuit against T-Mobile and its owners Deutsche Telekom and Softbank, calling for a reversal of the merger and for damages based on consumer overcharges. They allege that the merger was a violation of the Clayton Act, and that the combination also violated the Sherman Act by restraining trade.

Additionally, a group of wireless dealers have come together under a coalition called “Wireless Franchisees for Justice” to “call attention to the troubling treatment of T-Mobile’s dealers following the merger that was approved under false pretenses.” Basically, T-Mobile shut down lots of independent dealers after the merger, which is a classic monopolization move. Multiple firms have filed different suits against T-Mobile for the merger that was in their view essentially a fraud.

Now, could a break-up really happen? It’s hard to imagine it, but it’s not unprecedented. Last year, the fourth circuit upheld an order breaking up Jeld-Wen, a window and door producer that had bought a competitor and then started acting in ways meant to exclude competition. What made that case extraordinary is that it was brought by a private plaintiff, and yet it resulted in structural separation. T-Mobile-Sprint is obviously much bigger and more complex, but there’s the additional point that it’s clear the merging parties lied to the judge and there really can’t be any sort of sustainable remedy that will reset competitive conditions aside from a break-up.

Hopefully, this case goes to court, and part of the remedy will be clawing back the compensation that went to the executives for deception and monopolization. And frankly, the Department of Justice has an interest here as well; lying to the judiciary to get a merger through so you can overcharge consumers is wrong. And crime shouldn’t pay.

Weird Monopoly: Cineplex and Canadian Movie Theaters

Last week, Canadian movie theater giant Cineplex pissed off its customers by imposing a $1.50 booking fee for tickets purchased online and on its mobile app. The ostensible excuse was that it can ‘invest in digital infrastructure,’ but no one was buying it. In a functional market, consumers could just go to a different theater. But Cineplex controls the Canadian movie theater industry, with roughly 75% market share.

How does Cineplex maintain its power? The monopoly story here is pretty simple. Like the movie theater chains in the U.S. prior to the 1948 Paramount Consent decree, Cineplex wields its power by denying rival small theaters access to movies that people might wish to see. If it’s playing in a Cineplex theater, then it’s not playing in a small theater. This thread from an art house movie theater explains the conduct.

My guess is that the booking fee is designed to cheat the studios, since there’s usually a revenue split of the ticket price between studios and theaters. A booking fee is a way of raising prices without sharing.

Before Covid, the independents were trying to get the Canadian competition authority to go after Cineplex, but the pandemic shut everyone down and made the problem moot, at least for a time. Now, with both inflation and the return of in-person movie screenings, the controversy is returning.

At any rate, there is a bit of competition with Landmark in some areas, but if you want to either show or see a recently released movie in Canada, it’s fairly likely that you have to go to Cineplex.

What I’m Reading

Ernst & Young Fined $100 Million in Ethics Exam-Cheating Probe, Wall Street Journal

Private Equity Funds’ Claims of Strong Performance Are Based on a Mirage, CEPR

Democrats question Reckitt Benckiser’s plan to sell baby formula unit, Financial Times

In Colorado, “Low Wage” Now Means Six-Figures For Non-Competes, National Law Review

“Back to the Future” at the Federal Trade Commission: Highlights from an Expert Panel Discussion, American Enterprise Institute

North Dakota Attorney General's Office looks into Bill Gates-related farmland sale, AgWeek

Thanks for reading!

And please send me tips on weird monopolies, stories I’ve missed, or comments by clicking on the title of this newsletter. And if you liked this issue of BIG, you can sign up here for more issues, a newsletter on how to restore fair commerce, innovation and democracy. And consider becoming a paying subscriber to support this work, or if you are a paying subscriber, giving a gift subscription to a friend, colleague, or family member.

cheers,

Matt Stoller

P.S. After last week’s issue on inflation, BIG reader and economics researcher George Dibb sent me this excellent report on price hikes in the UK that his team compiled. It’s titled Prices and Profits After the Pandemic, IPPR.

New analysis shows that the profits of the largest non-financial companies were up 34 per cent at the end of 2021 compared to pre pandemic levels – rising significantly faster than inflation and wage growth. The analysis shows that this increase is being driven by a small number of companies, with 90 per cent of increases in profits accounted for by only 25 companies. The report argues that some firms could have considerable market power with very few competitors, and this could be making the cost of living crisis worse by raising prices beyond what would be economically justified. The report notes that there is a high degree of market concentration in some industries with the highest turnover.

The Jeld-Wen saga is the under-covered antitrust story of the last few years.

It's pretty much impossible to a build house or other structure without windows. The consolidation of window manufacturers and distributors in the Northwestern part of the US was leading to increased lead times for several years before COVID. Since COVID it's become an absolute disaster. Lead times on windows for even the simplest homebuilding project is now several months, with unclear delivery timelines.

The Jeld-Wen decision will, hopefully, help to alleviate this in part. But the fact that the consolidation in an important regional industry was allowed to happen at all was a tremendous regulatory failure with enormous downstream effects.

Stories about national phone carriers whose names are well-known to consumers are sexy (and important). But the really catastrophic choke points in the economy are largely hidden from consumers and involve businesses that supply other businesses.

It's not quite that simple. TMO was on the auction block for years before the Trump administration. AT&T was the best fit since they used the same signaling tech (Sprint and Verizon used a different tech), although today LTE and 5G are industry standards so that's no longer an issue. Legere was put in charge of a company that was doomed, so why not have a little fun? When his gamble worked out and then the merger with AT&T was blocked, suddenly TMO was in the catbird seat. The agreement had a penalty clause that gave TMO a big chunk of national spectrum, plus the 700MHz band they got from the LTE auctions.

Sprint, OTOH, had a lot of spectrum that wasn't as useful and were still behind on tech upgrades. Wall Street wasn't going to finance their network upgrade, so Softbank put them on the auction block. AT&T and Verizon weren't going to try because it was clear the FCC wasn't going to allow for mega-mergers (remember that during this time they blocked the Comcast acquisition of Time Warner cable systems), so they sat back. Meanwhile Sprint was late to launch LTE and had an eroding customer base.

But Sprint did have spectrum, and lots of it. Even if it wasn't in an ideal spot "on the dial," bandwidth is bandwith. They were in no position to use it. TMO was. And TMO had bigger plans than handsets. The holy grail these days is fixed point wireless (home Internet service). Basically replace your cable company with your wireless company. Solves the "last mile" problem, but requires a lot of spectrum/bandwith. AT&T and Verizon are using the 33cm band, which are very short range and directional frequencies. This means building out a network of "pico cells" in neighborhoods, fiber back-haul, etc. It will work but takes time and a lot of captial. TMO is using the spectrum they got from Sprint and AT&T, which is more like traditional handset spectrum in coverage, so they have a big short term advantange.

So yes your cell phone bill might be going up, but your cable bill might be going down. All the way down to $0. TMO is marketing $50/month for 250 Mbps service, no data caps, and self-install. If Sprint would have been able to roll out 5G on their own things might be different, but no player had enough bandwidth avilable to do it without building out a costly network.

Not saying it's right, but in a capital-intensive business if Wall Street isn't going to finance your tech upgrades you're going to wither and die. Softbank decided Sprint wasn't worth the effort. They could have sold to another equity firm, or a tiny cell company like Union Telephone, but then they'd be right back where they started, with a bunch of spectrum and no money to utilize it.