Fear and Consolidation in the Oil Patch

Fear and Consolidation in the Oil Patch

The consolidation wave among oil and gas producers, from Exxon-Pioneer to Chevron-Hess to Diamondback-Endeavor, is extreme. What's behind it? Will it affect gas prices? And what is the likely outcome?

Welcome to BIG, a newsletter on the politics of monopoly power. If you’d like to sign up to receive issues over email, you can do so here.

Over the past three years, the anti-monopoly movement has succeeded in tamping down mergers across nearly every part of the economy, except in one conspicuous place. Oil and gas, where there has been an explosion of consolidation since the end of last year. And that’s what I’m writing about today. Oil and gas is not a sector I know well, but I’ve been doing interviews with industry participants, and these are my main take-aways about what’s happening.

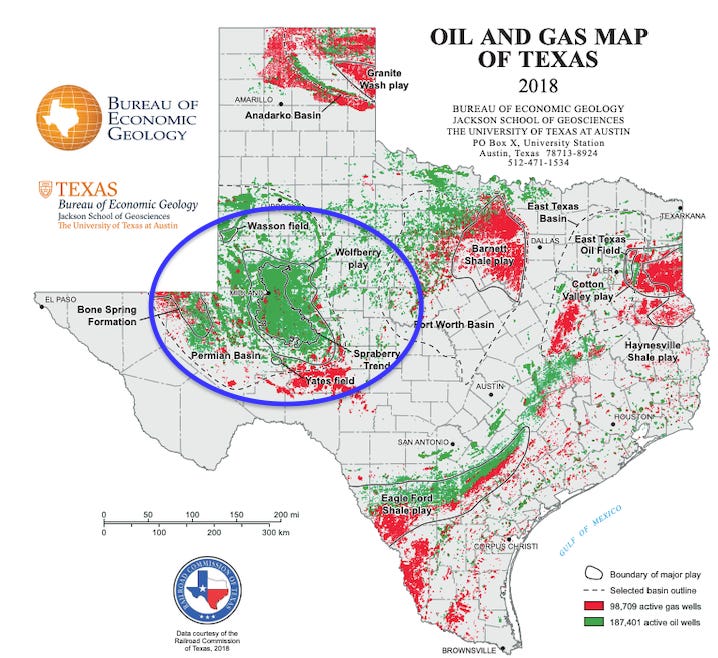

When you talk to longtime oil and gas experts, there’s a level of awe that comes over their voice when discussing the Permian Basin in Texas. And for good reason. Over the past hundred plus years, since drillers struck oil in Spindletop, the first ‘gusher’ in history, Texas has been drilled, poked, prodded, and drilled even more, in every way shape or form, until you would expect nothing could come out of the land. America, apparently, hit peak production in the 1970s, and would henceforth be dependent on the vagaries of Saudi princes.

But since the mid-2000s, and the explosion of a new form of drilling - hydraulic fracking, in which drillers inject pressurized liquid into a rock formation to crack it and release oil and gas, the Permian has again become one of the great global oil and gas phenomenons, with that field alone producing more oil than Venezuela and Iraq. Along with Eagle Ford, it has made Texas once again a major energy exporter, a swing producer with geopolitical power. In World War II, the U.S. oil surplus powered the allied victory, in 2022, the U.S. natural gas surplus substituted for the Russian gas pulled off the market during the invasion of Ukraine. (As an aside, if Biden wins reelection, he can probably thank drillers in the Permian for bringing gas prices down.)

Texas is one of the birthplaces of populism, with a group of ranchers coming together in 1875 in Lampasas County, Texas to form what later became the National Farmers' Alliance and Industrial Union, who opposed what they perceived of as predatory interests of concentrated Eastern capital. In the 20th century, oil and gas became a core part of that story. Congressman Wright Patman owned oil-producing land, and the Texas Attorney General in the 1930s spent a good deal of his time suing Standard Oil for antitrust violations so as to keep the oil and gas in Texas under the control of Texans. The great scholar of the farmer coalitions of the 1880s and 1890s, Lawrence Goodwyn, wrote his last book on the independents of Texas, Texas Oil, American Dreams, chronicling the Texas Independent Producers & Royalty Owners Association, which preserved the ability of ordinary people to be a part of the industry and share in the resources throughout the 20th century.

But since the 1980s, it is high finance that has dominated thinking among Texas oil producers, rather than the traditional notion of having some producing wells on your property financed by the local wealthy establishment of doctors and lawyers. As in much of America, the traditional hostility to concentrated corporate power died away, though if you peel under the surface, it’s still there. Still, along with the fracking revolution came hedge funds and private equity, and a new business model. The idea was to hire a geologist, a landman to go through court records, engineers, and some drilling specialists, and then lease as much acreage as you can. You’d drill a few wells, prove you have reserves, and then flip the land to a larger player with more financial backing. It was always a consolidation play. And last year, it hit the end stage.

In October of 2023, Exxon, one of the biggest integrated oil firms, announced it would buy Pioneer Natural Resources for $59 billion, which was quickly followed by tie-ups between Chevron and Hess ($53 billion), Occidental Petroleum and CrownRock ($12 billion), Diamondback and Endeavor ($50 billion), and Chesapeake-Southwest ($7.4 billion). Other notable deals included Exxon-Denbury ($6B), Ovintiv - Black Swan, PetroLegacy, Piedra Resources ($4B), Permian Resources-Earthstone ($4.5 billion), and Civitas buying $7 billion of assets in the Permian. That’s a little less than $200 billion in mergers.

In every part of the industry, this consolidation is the topic of endless amounts of gossip, with employees counting up their stock options, oil field service workers fearful of what this might mean for their leverage, and everyone wondering what it portends for the future. This consolidation is a fundamental reordering of the domestic industry. As the FT put it, “Half of the sought-after Midland sub-basin, which makes up the eastern part of the Permian, will be controlled by just two companies: ExxonMobil and Diamondback.”

What’s driving most of these acquisitions? There are two trends. First, it’s getting harder to increase production in the Permian Basin, as well as other areas in the U.S. with significant amounts of fracking, so the price of good acreage where you can drill for oil and gas is going up. And second, the large public corporations and private equity firms financing most production want to have as their ‘narrative’ a story that they have access to reserves. “Since investors are closely scrutinizing inventory life when valuing oil-focused E&Ps,” wrote one analyst on an oil and gas merger by Ovintiv, “adding the additional locations should help the company improve its equity multiple and rerate higher.”

So what will be the consequence of these mergers? To understand that, you have to know a bit about how an oil and gas company is structured. When you hear about a company like Diamondback or Pioneer, which is known as an E&P company (exploration and production), you might imagine a firm with lots of roughneck oilmen, geologists, guys poring through records looking for acreage, and drillers, and so forth. But that’s more a mirage, large oil companies operate like real estate firms. Just as those real estate firms outsource most of the ‘doing’ to a property management company, big oil operators outsource most of their work to oil field service companies, develop land, drill it or frack it, bring wells into production, do ongoing maintenance, and so forth. There’s consolidation in these firms too, and the big service companies - Halliburton, Schlumberger Baker Hughes, NOV Inc - are themselves children of roll-up strategies. (Pipelines are usually owned by Enterprise, Kinder Morgan, etc, with storage owned by a different set of companies).

Oil field service jobs are good jobs, among the last remaining - highly skilled, technical prowess, more than six figure earners, that high school graduates can get. And there are a lot of E&P companies, big, medium, and small, and they are constantly buying and selling wells and acreage to one another. There is a tremendous amount of innovation in this space, and there has been ever since the fracking boom in the early 2000s. Pioneer Natural Resources, for instance, which was a small company twenty years ago, is responsible for some of the technological innovation in fracking. It’s an extremely sophisticated technology space, with the ability to create new tools, drills, valves, software, piping, or new deployment techniques and increase the barrel of oil per worker produced. Data scientists in the space make hundreds of thousands of dollars, and the software architecture is built by Palantir or a Silicon Valley firm.

BIG is a reader-supported newsletter focused on the politics of monopoly and finance. This is journalism and advocacy that challenges power, so please consider a paid subscription. Lies are free, the truth costs a few bucks. You can subscribe by clicking here.

So one very obvious consequence - and everyone I talked to agreed on this - is that suppliers are going to get squeezed out of the space. Think of a 60 person downhole tooling company, if a mom and pop company has Chevron and Hess as customers, now they only have one customer. They are still serving the same amount of wells, they just have less pricing power. One oil engineer pointed out Exxon thinks it can wring out $2 billion in ‘synergies’ - aka cuts to supplier payments - just from its Pioneer buy. That said, this dynamic doesn’t mean that these oil field service firms will all object to consolidation. If that same firm has only Chevron as a customer and not Hess, they might now think that Chevron will buy more from them. Or they might assume they can sign a long-term contract, and avoid losing pricing power, since they think the Permian is such a powerhouse it won’t matter. After all, if there’s oil underneath, someone’s gonna invest. Whether to keep a well going is simply a function of the price of oil, and whether that price is higher than the cost of a well.

Will this reduce the amount of oil and gas production? Well, if firms can squeeze out supplier margin, that lowers the cost of a well, and fosters more production. But fewer oil field service firms with less margin will in turn reduce innovation, which could mean the opposite. The explosion of E&P firms since the 2000s has led to a healthy ecosystem of domestic firms, if E&P firms consolidate, then innovation may move from Dallas and Denver to Dubai.

And then there's the fact that the big players are more high finance than oilman, and their strategies are driven by Wall Street. There’s a lot of overpaying by the majors for acreage, simply so a CEO can tell an analyst, “I've got 50k acres in the middle of Eagle Ford,” the same way that firms tried to mimic Uber and WeWork by losing money to gain market share in the mid-2010s. Here’s where it seems like reduced production is the likely consequence. The Dallas Federal Reserve asked E&P firms about their goal in 2024, and it’s a pretty stark bifurcation by size. The small ones want to produce more, the big ones want to engage in mergers.

Consolidation will have effects on a bunch of other stakeholders in the industry. If oil field services companies shrink or are now beholden to a few large E&P firms, then it’ll be much harder to make it as a smaller player because of what’s called the ‘waterbed effect.’ If there's only a handful of companies doing some essential service, and they are under contract to, say, Exxon, then Exxon can turn around and squeeze its rivals. “Sorry we’ll get to you in 2026” will be the mantra if you own some wells and need specialized drilling or maintenance. This dynamic is similar to a small grocer that needs to get toilet paper during the pandemic, when Walmart has mandated that it gets first dibs on everything produced by Kimberly-Clarke. And then there’s the ‘bully mentality’ of many of the big players, especially firms like Chesapeake, which often doesn’t pay royalties to landowners unless forced to by a court.

These mergers are happening in a backdrop of the pandemic and post-pandemic moment, as firms in high-profile ways were very explicit they would not drill more to bring down oil prices. Pioneer’s Scott Sheffield, for instance, said that “everybody's going to be disciplined, regardless whether it's $75 Brent, $80 Brent, or $100 Brent," according to publication Hart Energy. "All the shareholders that I've talked to said that if anybody goes back to growth, they will punish those companies.” He added, “Whether it’s $150 oil, $200 oil, or $100 oil, we’re not going to change our growth plans.” And certainly, Senator Chuck Schumer and 20 Democratic Senators jumped on comments like this and argued that the Federal Trade Commission should block various oil mergers, because it will reduce production and increase oil prices.

That said, I don’t know that it’s even possible for small changes in domestic production to change the price of oil globally. Moreover, in some ways, there’s a lot less rationality in these comments than there is in Wall Street trends. In 2020, oil prices were so low that frackers pledged they would never increase production, even as prices went up. But it’s 2024, and, well, production is at a record high. Still, there is a good legal argument against oil and gas consolidation, which is not that oil prices will go up, but that compensation to oil field services firms and workers will go down, and innovation will decline. That’s what is called a ‘monopsony’ claim, and it’s similar to the successful case the government pursued in the Penguin/Simon and Schuster book merger, where enforcers argued that removing a bidder from auctions for book advances would lower payments to authors. With dozens fewer E&P firms, it’s hard not to see reduced competition for oil field service firms.

On a more basic level, one land man told me a good story. There used to be many large independent operators in Corpus Christi, 10-20 of them, who would bring in local doctors and attorneys who wanted to invest. They'd invest in the wells and put a lot of money into their pockets. Now it's all hedge fund money, with no spreading of the wealth to local business leaders, and just three independent operators. Does that mean the FTC can step in and stop the reorganization of this industry? Well, that depends. I don’t know if Texas judges would look kindly on a Democratic FTC coming in to try and stop mergers in the oil and gas industry, unless there’s local dislike of consolidation as well. So the open question is whether there is any coherent industry opposition to these mergers. After all, if everyone in an industry basically thinks that consolidation is good, then it’s hard to get witnesses who will tell a judge otherwise. It is definitely not the case that industry participants are all excited about dealing with an industry of giant bullies. There was a time Texans would have realized they have rights through the antitrust laws to share the wealth. As the industry consolidates, is that merely a distant memory?

Thanks for reading! Your tips make this newsletter what it is, so please send me tips on weird monopolies, stories I’ve missed, or other thoughts. And if you liked this issue of BIG, you can sign up here for more issues, a newsletter on how to restore fair commerce, innovation, and democracy. And consider becoming a paying subscriber to support this work, or if you are a paying subscriber, giving a gift subscription to a friend, colleague, or family member.

cheers,

Matt Stoller

I’ve been waiting for this piece!

Great article Matt. Lots I disagree with, but well written nonetheless.