Government Stupidity Is By Design

Government Stupidity Is By Design

Unwinding forty years of booby trapped bureaucracies takes time, but it's happening. And the billionaires are noticing.

Welcome to BIG, a newsletter on the politics of monopoly power. If you’d like to sign up to receive issues over email, you can do so here.

Legendary Congressman John Dingell once let slip the dirty secret about power. “If I let you write the substance and you let me write the procedure,” he said, “I'll screw you every time.”

Today I’m going to write about a little-noticed procedural change by antitrust enforcers that caused the lawyers who represent every large corporation, every foreign government, and every large private equity fund to scream in unison.

The goal of this change is to get the government to stop acting so stupidly when it comes to corporate power. Almost no one outside of the billionaire servant world noticed this shift when it was announced, but as it turns out, making public bureaucracies act competently is a threat to very powerful interests who rely on such institutional blindness.

In other words, if you want to know why the government is so clumsy and stupid, this issue is for you. I’m even going to show you a way that you can help fix the problem, without much effort.

First, an announcement. My organization is hiring, so if you want to do anti-monopoly work, please apply. We have an opening for a senior communications role, a junior communications role, and an operations role. If you dislike monopolies and want a new job, check out the descriptions and see if they are right for you.

And now…

How to Make Corporate Lawyers Extremely Unhappy

Six weeks ago, the government put out an anodyne press release, designed to put normal people to sleep. It was titled “FTC and DOJ Propose Changes to HSR Form for More Effective, Efficient Merger Review,” and it was accompanied with a long and equally boring notification in the Federal Register, which is the official journal of the U.S. government. The Federal Register publishes hundreds of pages every day, full of announcements of new rules and minor changes to government forms. Most days, it’s not something to pay attention to.

But something about this one was different.

Immediately, corporate lawyers started complaining, especially those who focus on helping the multi-trillion dollar private equity industry buy and sell companies. “This is breathtaking and astonishing in its reach and potential impact to deals,” said James Langston, a partner at Cleary Gottlieb, a firm that represents Google, as well as private equity giants KKR and TPG. "It's a huge change,” according to Deidre Johnson, an antitrust lawyer at Ropes & Gray, whose clients include Bain Capital, Silver Lake Partners, and Thomas Lee Partners.

“If adopted, these proposed changes will have a dramatic impact on merger filings in the United States,” said one law firm. “An already robust, time consuming and expensive process will become exponentially more challenging.”

When something significant happens, these law firms send out alerts to clients. And oh, did the client alerts come, in a flood. “Burdensome.” “Sweeping.” “Idiosyncrasy.” “Dramatic.” The words are muted but full of passive aggressive rage, authored as they were by extremely angry multi-millionaire lawyers who often help their clients skirt the law. And here are some of the firms that sent out such breathless, angry notices. Wilmer Hale. Steptoe. Kirkland and Ellis. Dechert. Wilson Sonsini. Sullivan and Cromwell. Covington & Burling. Etc.

These names may or may not be recognizable to you, and may sound like 19th century shipping firms trying to sneak opium into China. But in the legal world, these law firm brands are as recognizable as Coke, Pepsi, Apple, or Google. Every single major corporation, bank, foreign government, and private equity firm has one or many of these law firms on retainer, which means that every single CEO or general counsel at each and every one was alerted about this change, probably multiple times.

And if that’s not enough, the Wall Street Journal editorial page, read by many billionaires, immediately went on the attack.

This is a very big reaction, just for changing a filing form. So the question is, what did the antitrust enforcers actually do to inspire such rage?

Cardboard X-Ray Glasses Don’t Work

As it turns out, the change is relatively simple. The Federal Trade Commission and Antitrust Division are requiring big corporations and private equity funds who want to engage in big acquisitions to actually tell the government what they are doing. That’s it. That’s the change. Merging firms will soon have to fill out basic questions, such as “Why are you merging?” “Who is on your board of directors?” And “Who are the major creditors and investors in this merger?”

If that sounds obvious, a sort of ‘well shouldn’t they be doing that already?!?,’ well, you’re not wrong. In 1976, Congress passed a law known as the Hart-Scott-Rodino Act (HSR) mandating that companies notify the government upon any attempt to buy a company. In 1978, the FTC came out with an HSR form for firms to fill out, mostly a check-box type exercise to ensure they were paying the government filing fee.

The structure of the form didn’t seem like a big deal at the time. Only 150 firms a year even had to file this form, because mergers just weren’t common. But today, there are about 3,000 qualifying mergers a year, a little over nine major transactions every day. Imagine you’re a government lawyer, and you are handed a separate transaction in an industry you know nothing about, and you have to decide within three hours or so whether to take legal action.

The effect of this resource and information mismatch is that a lot of mergers just slipped through. For instance, when Discovery bought Time Warner in 2022, further consolidating Hollywood, there was a lot of frustration the Antitrust Division let it move through without a challenge.

“I lost my job thanks to the Warner Brothers-Discover Merger,” wrote animation director Kelsey Norden. “When the merger was complete, [Discovery CEO David] Zaslav started cutting countless shows from production, even those that were nearing completion. My show was one of those... I've been struggling to find full time work ever since, since so many studios are following WB's suit and axing shows from their production schedule.”

The Antitrust Division didn’t try to block the Discovery-Time Warner merger, and one key reason is they probably didn’t have data on how it would affect creators, or sub-markets like animation. Indeed, Discovery has a bunch of competitors in TV, so you could say maybe it’s not an obvious monopoly there. However, Discovery does own and control most non-scripted TV, aka reality shows, and that’s a separate sub-market it does control. It’s unlikely the antitrust lawyers tasked with this deal knew that, or even knew to ask. And so the merger went through, unchallenged.

We’ve seen this dynamic over and over. Earlier this year, insulin cartel member Sanofi bought Provention, rolling up a small part of the insulin market, which will lead to higher prices and more leg amputations. One analyst, horrified, privately asked me, “how the Federal Trade Commission could let that happen?” I’m guessing that the FTC lawyers simply didn’t know what Provention did, and Sanofi hid it from them enough to move the merger through.

The number of such mergers is endless. Small dialysis firms. Fertility clinics. Landscaping. Street sweeping. Etc. In 2019, mining giants Barrick and Newmont consolidated 75% of the gold market in Nevada to form a corporation called Nevada Gold Mine - the new monopoly quickly got rid of the union. In 2019, a private equity firm rolled up all three major mail sorting software firms, without anyone noticing. Employees involved were baffled that no one in D.C. was looking.

Cynicism about politics in the U.S. is rife, for good reason. And there are certainly grounds for thinking the game is rigged. But one of the reasons that the government doesn’t stop these mergers, or many others, is simple. No one in the antitrust agencies knows what is happening. If you work in the industry, you know, but why would anyone assume antitrust lawyers would? They aren’t Gods, they are smart lawyers in an understaffed agency responsible for mergers in a $24 trillion economy. And the reason for this blindness is intentional, rooted in the poor design of the form meant to notify the government of corporate combinations.

With the old form, corporations didn’t have to list subsidiaries. They didn’t have to tell the government why they were merging, or who was on their boards of directors. They didn’t have to give the merger timeline, or if there was foreign money involved. They didn’t even have to describe the acquiring firm, only the target firm. They had to turn over internal documents about the merger, but only final drafts, which meant they knew how to hide documents from enforcers. It’s not that the old forms required no work, firms had to provide a bunch of useless data about where they fit into the economic Census. The old form was the equivalent of being told to do an X-Ray and being given cardboard X-Ray glasses from the 1950s.

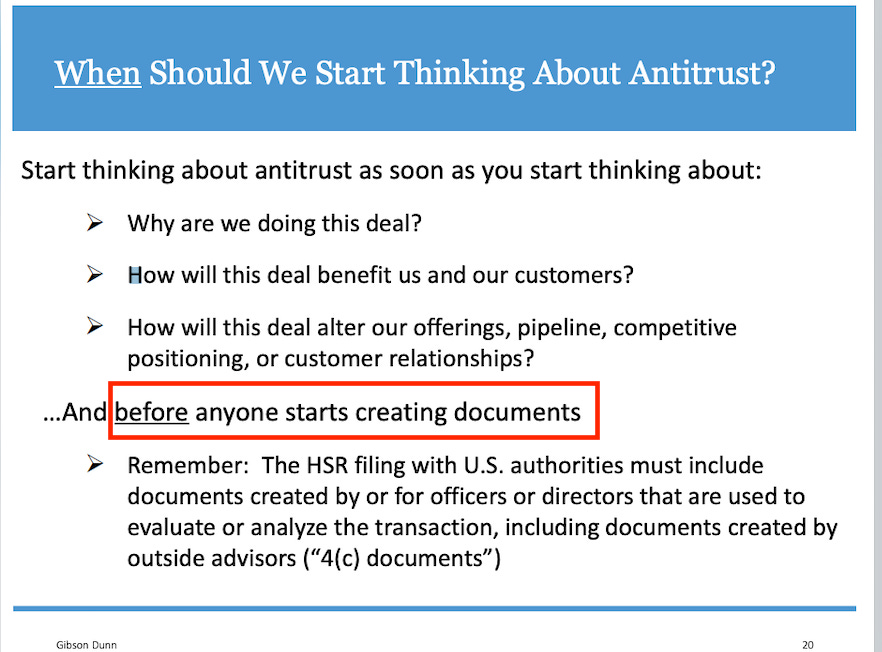

The government was blind, and deal-makers liked it that way. (Indeed, here’s a slide from biglaw firm Gibson Dunn marketing their antitrust services to prospective clients. I highlighted the bit in red, which makes it clear what these antitrust lawyers really do.)

Getting an Actual X-Ray Machine

The new draft form is like actually getting an X-Ray machine. With the new form, merging firms must explain *why* they are doing the merger, along with documentary evidence supporting the rationale. Most mergers have a strategic purpose, so now they will have to describe already-existing relationship between the firms, competitive overlaps, and related transactions. Often, financiers in mergers stay out of sight but exercise industry-wide control. So this new form requires firms to describe the private equity investors, foreign governments, and creditors that might have power in the deal, as well as the corporation’s subsidiaries, board members, and entities in which they have more than a $10 million investment.

There are a few other core changes. Mergers are often part of a series, so now firms have to list all acquisitions they pursued in the past five years. Firms must list the defense or intelligence contracts they have, as well as labor law violations, because those could indicate increasing control of labor markets as a rationale for the deal.

That might seem like a fair amount of work, but it’s not. It’ll require an additional 144 hours, which is three and a half weeks for one lawyer. And truth is, it’ll probably help the companies themselves, because most mergers are poorly prepared, This new form will actually force CEOs to think through aspects of their deals they hadn’t considered. It’s a bit like putting up a sobriety check on Saturday nights in an area with a lot of nightclubs. Sure it’s a pain, but drunk driving, like big mergers, are often harmful to the people doing it, as well as their victims.

BIG is a reader-supported newsletter focused on the politics of monopoly and finance. If you haven't done so already, please consider supporting this work by upgrading to a paid subscription. The truth costs a few bucks, but in the long run it’s much cheaper.

Let’s Make This Happen

The agencies put out this form, and it’s now available to read and for public comment. That means anyone can actually tell the government what they think about it. Usually only lobbyists and lawyers working for billionaires do that, because, well, only lobbyists and lawyers working for billionaires notice these kinds of changes. But now I’ve told you about it.

And if you want to submit a comment, you can do that here. There won’t be many comments in this docket, so your voice actually will matter. I would specifically recommend that you talk up the need to collect data on labor markets, because that’s something that seemed to particularly offend much of the antitrust bar. But say whatever you want.

Broadly speaking, it’s been two years and change since new leaders of the antitrust agencies took over, and it’s certainly been fascinating. The old consensus is dead, a new consensus isn’t here yet. On the plus side, we have been able to put a real dent in mergers, and made significant gains in consumer protection. On the minus side, there have been legal losses, and attempts to split apart companies are taking a long time. Many judges have been hostile, as have journalists.

But on a more narrow level, we’re discovering a legacy of booby traps in the enforcement agencies placed there by a generation of political leaders who adhered to the old consensus. The useless HSR form was one of them. Working through these takes time, but it’s a key part of getting the government to actually see the economy the way it really is.

Thanks for reading! Your tips make this newsletter what it is, so please send me tips on weird monopolies, stories I’ve missed, or other thoughts. And if you liked this issue of BIG, you can sign up here for more issues, a newsletter on how to restore fair commerce, innovation and democracy. And consider becoming a paying subscriber to support this work, or if you are a paying subscriber, giving a gift subscription to a friend, colleague, or family member.

cheers,

Matt Stoller

I just submitted a comment to the filing citing the need to bring more transparency into the merger process, prevent anti-competitive behavior and collect data on the labor market.

It seems like you have to do more paperwork to build a granny flat in an average-size American town, than you do to justify a merger of billion-dollar companies, at least on the existing model.