On Inflation: It's the Monopoly Profits, Stupid

On Inflation: It's the Monopoly Profits, Stupid

A raft of studies have come out showing that this inflationary episode is being driven by the supply side. Policymakers are responding.

Welcome to BIG, a newsletter on the politics of monopoly power. If you’d like to sign up to receive issues over email, you can do so here.

With Fed Chair Jay Powell testifying today and tomorrow in Congress about inflation, I figured it’s time to revisit the reasons that prices are increasing. As the debate moves onward, economists are starting to look into market power as a causal factor, and some policymakers are beginning to regulate markets as a solution. It’s not quite enough to fix the very serious problems we’re facing, but we’re beginning to see an outline of what a new model of economic management might look like.

The Hoary Wage-Price Spiral

For years, the thinking behind inflation is that the primary culprit behind price hikes had to be wages. After all, labor is a huge component of input costs. Higher wages led to higher costs and prices, which meant workers demanded more, which meant higher costs and prices, and so forth. That was called the wage-price spiral, and the wage-price spiral analysis is still at the heart of the debate over inflation. The Fed sees lower wages as a victory for its mandate to stop inflation, and the stock market goes up when wages decline. The problem, however, is that in this highly inflationary period, real wages are actually going down, falling by 3.5% over the last 12 months. If that’s true, then there can’t be a wage-price spiral. So what is going up?

Well, profits.

Back in December, as this debate was first raging, I did a rough calculation, and showed that 60% of the increase in inflation was going to corporate profits. I was, along with others in this debate, trying to show that there’s a profits-inflation spiral. Such a claim generated deep anger among the neoclassical economics establishment, who largely subscribe to the argument that inflation is almost entirely a monetary phenomenon and cannot be a result of factors like market power in individual markets.

But the profit contribution to inflation is too obvious to deny. Lindsay Owens at the Groundworks Collaborative, a nonprofit, has been tracking investor calls, and laid out how CEOs routinely bragged about elevated pricing power. And over the past week, several papers have come out essentially confirming the original profits-inflation analysis.

The supply chain element should be obvious; pricing changes first showed up in terms of shortages. I had been warning about supply shortages since late February of 2020, noting that such shortages are a result of both excess market power and removing rules over public utility sectors of the economy, like transportation. (Here’s my piece on shortages in health care and baby formula, which is still the only write-up linking the two problems.) In 2021, I recommended an excess profits tax, tighter price-fixing rules, re-regulation of certain areas, and suggested that economists needed different models that went beyond simple links between interest rates at the Fed and changes in pricing. These were not my ideas, many others suggested similar notions, and it’s all basically copying what we used to do when our public institutions could actually understand markets.

Fortunately, a lot of policy changes are happening along the lines we recommended, though these shifts are quiet. All over the world, policymakers are using excess profits taxes and price gouging rules. In the U.S., Pennsylvania is considering stronger price-fixing laws. The FTC is investigating price discrimination by dominant firms, and Rohit Chopra at the Consumer Financial Bureau is cracking down on various junk fees charged by banks, which drain tens of billions of dollars from consumers. Most importantly, Congress actually passed a law re-regulating ocean shipping, and Biden signed it.

These policies are having an impact. Take the Ocean Shipping Reform Act. Ocean shipping is fundamentally a public utility service, a network system requiring interoperability of ships, equipment, and ports, but it is regulated as if the shipping lines are competitive sellers of ice cream. Over the past 20 years, this mismatched regulatory model distorted shipping, leading to Too Big to Sail boats and when the pandemic hit, private tariffs of between 10-20%. Fortunately, because of this new law, the consolidated ocean carrier sector is being forced to stop predatory fees on shippers, as well as to allocate shipping capacity to agricultural exports. That’s excellent. Policy works. (Now it’s time to re-regulate railroads, trucking, and airlines, who are all having similar problems.)

Aside from policy shifts, economists and analysts are rethinking the relationship between individual markets and the broad changes in inflation. That there is some sort of relationship between the pricing power of firms and prices in the economy writ large should be obvious, but the macro Gods of economics refused to consider it. Here’s Larry Summers in late December, with a tweet that prompted me to write my original piece on profits and inflation.

Jason Furman, Obama’s chief economist, has also been an important voice against the idea that market power is a driver of inflation. But while these economists have intimidated Biden, they have not stopped the onslaught of research. The first crack in the macro temple was in January of 2022, when economists at the Fed looked at industries dependent on semiconductors, and found those industries increased prices by 40% more than non-dependent ones. This paper wasn’t attacking the wage-price spiral, but it does link semiconductors to price increases.

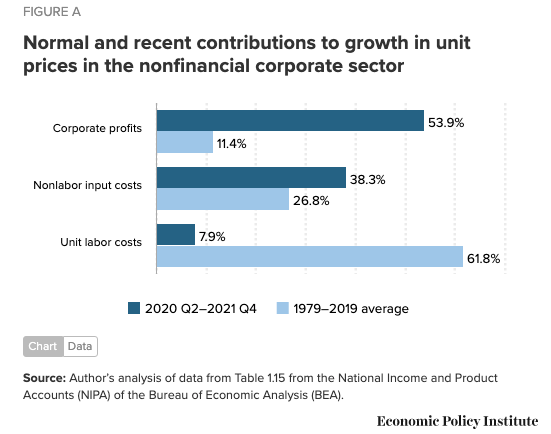

In March, 2022, economists at the Federal Reserve of Boston did a report on consolidation and inflation, concluding more directly that “the increase in industry concentration over the past two decades could be amplifying the inflationary pressure from current supply-chain disruptions and a tight labor market.” The response from certain traditional antitrust economist types was to refuse to accept the data. But then in April, there were two more papers on the problem. Antitrust economist Hal Singer showed that firm concentration levels and price increases were correlated. And Josh Bivens at the Economic Policy Institute did a great analysis of inflation and profits, illustrating that wages, far from increasing inflation, are actually holding it back.

Price hikes, he noted, were going to profits.

The analyses are continuing, and we keep learning. This month, economists at the Federal Reserve Bank of San Francisco noted that supply problems were driving about half of the increase in inflation, versus demand, which drove about a third of the increase. Here are the charts they put out.

There are two interesting elements of their analysis. First, the demand side was the government spending and low interest rates from the Fed, which is what angered Larry Summers. This stimulus is petering out. Second is how the SF Fed defines “supply-driven.” They write, “Supply-driven categories are identified as those where unexpected changes in price and quantity move in opposite directions.” Basically, if quantity goes down and price goes up, that’s a ‘supply-driven’ category. Supply is framed as an unforeseen pandemic-related disruption, akin to the weather. But in fact, lower output and higher prices is also textbook monopoly pricing behavior. Now, are all instances of lower output and higher prices in this pandemic a result of monopoly power? No. But are all instances of lower output and higher prices in this pandemic a result of pure disruptions divorced from market power? Also, no.

BIG is a reader-supported newsletter focused on the politics of monopoly and finance. This is journalism and advocacy that challenges power, so please consider a paid subscription. You can always get lies for free. The truth costs a few bucks, but in the long run it’s much cheaper.

And this leads us to the problem of monopoly profits, the basis for my original observation about all those nice new profits in this inflationary period. Status quo proponents offered two basic objections to the inflation-profits theory. First, the skeptics argued, there wasn’t some significant increase in concentration in 2021, in fact consolidation has been a thirty year problem. So why would inflation suddenly start in 2021? And second, firms with the most pricing power, like big tech or big pharma, were not really the ones raising prices during the pandemic. So consolidation couldn’t be driving price increases. In fact, consolidation could be absorbing price increases, as firms with lots of margin can afford not to raise prices.

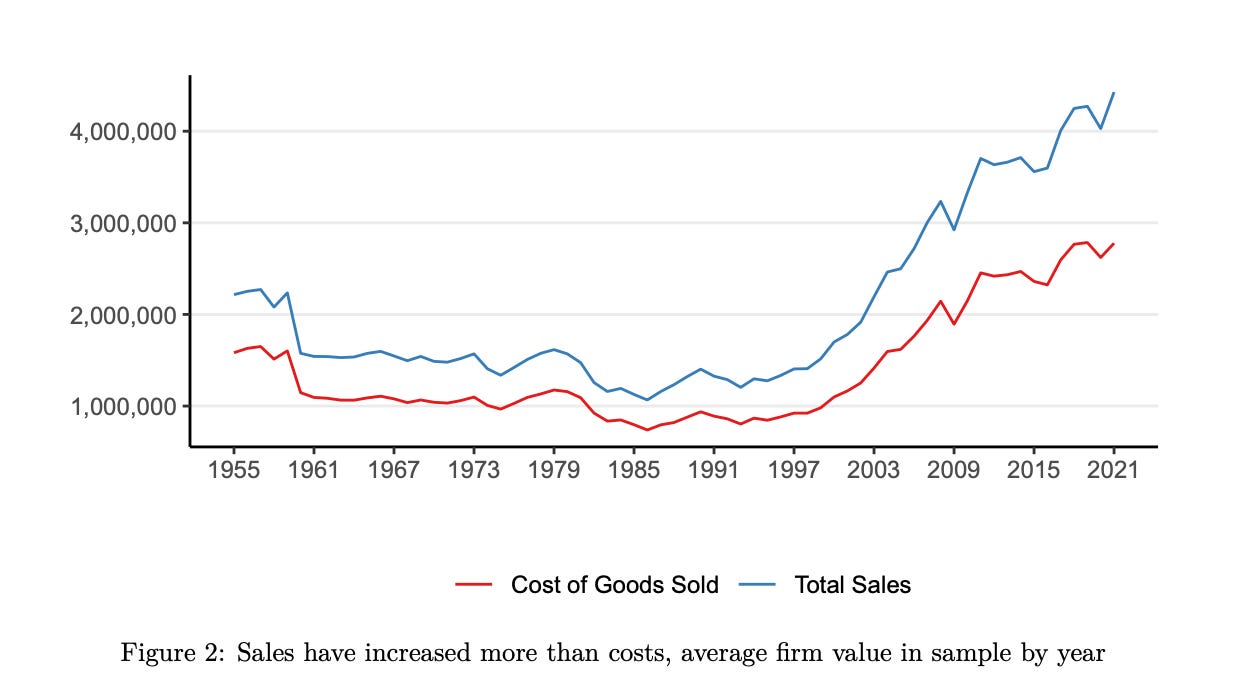

To answer these, I’ll refer to a new paper by Mike Konczal and Niko Lusiani at the Roosevelt Institute titled “Prices, Profits, and Power.“ Their thesis is that corporate markups, which is the price firms sell goods above marginal cost of producing those goods, have skyrocketed during the pandemic, and that the industries exploiting markets have changed. Konczal has traditionally been a deep skeptic that monopoly power is a policy problem, so when he co-authored this paper, I took note. Here’s their thesis, in a chart. Basically, costs are up a bit, but prices are up far more than costs.

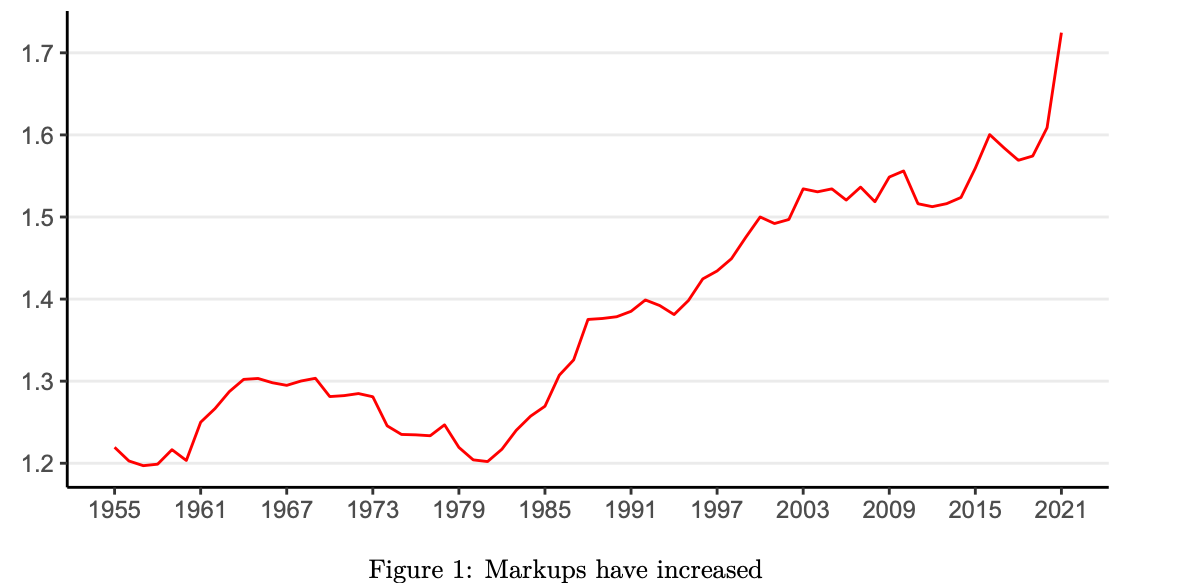

Their paper answers the two basic objections of the skeptics. First, they show that while concentration might be a longstanding problem, firms exploited their power more during the pandemic with a dramatic increase in markups. The increases in 2021, they write, were “both the highest level on record and the largest one-year increase—over 2.5 times the increase of the next several largest annual increases.” Here’s a chart from their paper demonstrating as much.

Moreover, they found that firms at the top of their industries, and bigger firms, got bigger markups, possibly because firms with less competition might have been “able to take advantage of one-time demand and supply shifts in 2021 to increase their markups further during the pandemic.”

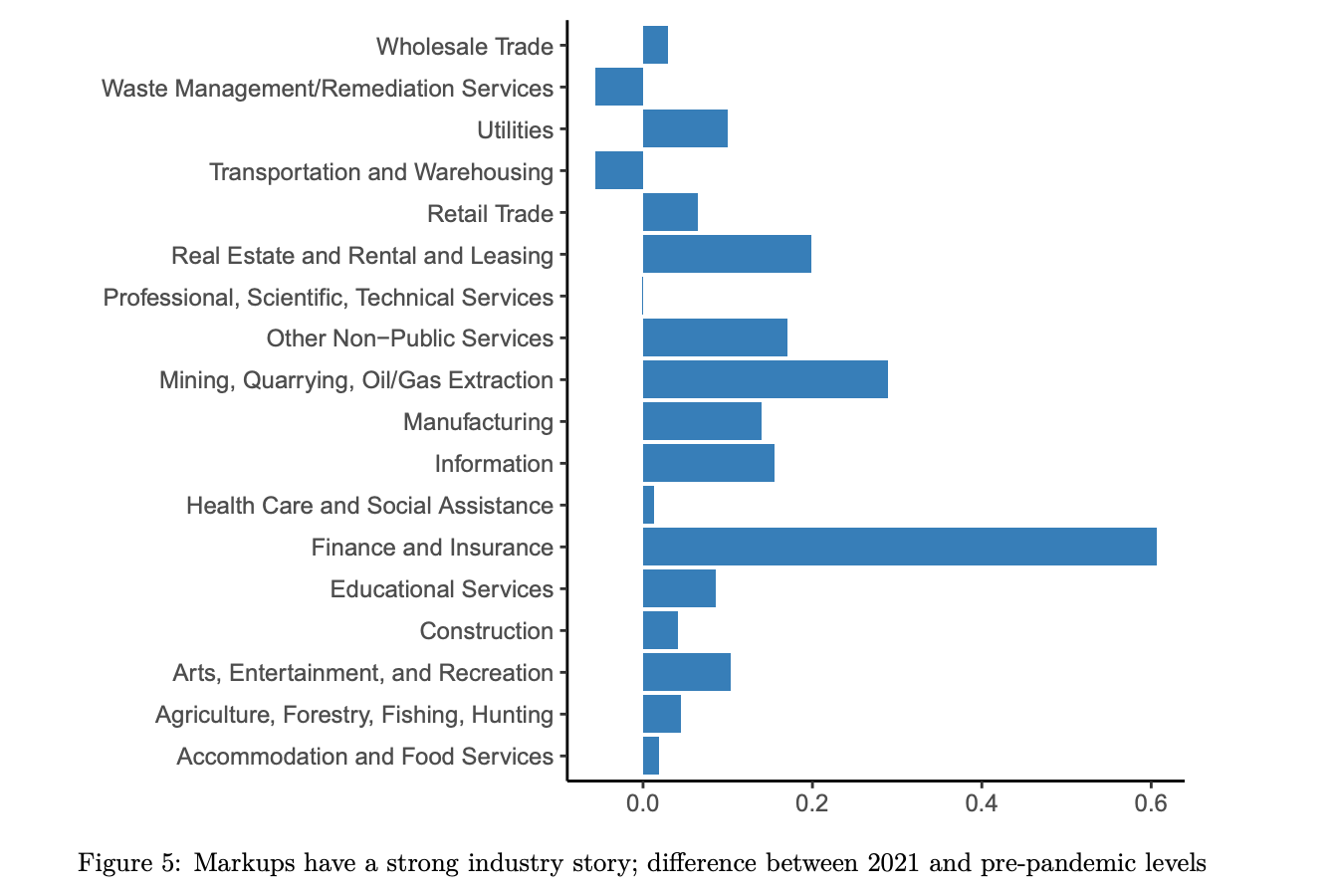

Second, Konczal and Lusiani showed that there was a significant change in mark-ups not just among firms within industries, but between industries as well. Oil and gas did very well, health care did not. Here’s their chart showing what happened.

For decades, there hasn’t been a big shift in markups between industries. But that changed during the pandemic, because the pandemic and the policy response itself shaped who could profit. Big pharma wasn’t in a position to profit, but oil refineries were. While not every firm with market power raised prices, market power could still elevate profits in other industries.

Ironically, while this analysis might lead some to think that the Fed shouldn’t be raising rates and drawing down its balance sheet, I draw the opposite conclusion. If you look at the most potent industry markup, you’ll see it is not what you’d expect from a pandemic, like transportation or health care. It’s finance/insurance. Number two is oil and gas, a heavily junk bond fueled industry that shut refineries and has less capacity than it did in 2019. Number three is real estate and rentals. In other words, the most financialized sectors of the economy are the ones most adept at exploiting pricing power during the pandemic. That is likely a result of cheap money from the Fed sloshing around Wall Street, or what I wrote up as the Cantillon effect. That needs to stop.

Regardless, supply side measures focused on individual markets, like antitrust, regulatory policy, industrial subsidies to re-shore supply chains, and ending cheap capital for Wall Street are the key ways to address inflation. But reducing government spending or further lowering wages for workers, while they could work, aren’t hitting the drivers of the problem. This debate isn’t over, and as we learn more about how our economy really works, it won’t be for some time.

Thanks for reading!

And please send me tips on weird monopolies, stories I’ve missed, or comments by clicking on the title of this newsletter. And if you liked this issue of BIG, you can sign up here for more issues, a newsletter on how to restore fair commerce, innovation and democracy. And consider becoming a paying subscriber to support this work, or if you are a paying subscriber, giving a gift subscription to a friend, colleague, or family member.

cheers,

Matt Stoller

P.S. Earlier this month, I wrote up how Apple was trying to block antitrust by encouraging a Federal privacy bill to confuse things in the Senate. Senator Maria Cantwell, who chairs the Senate Commerce Committee, said there is no way the privacy bill in its current form is advancing. So that threat is gone.

Hmm - I thought that inflation is created by printing money...

Thanks Matt.

As I've commented a few times on these, what was missed about corporate concentration and markups is that constrained markets (e.g. demand increasing faster than supply) are exactly how large markups get exercised in practice.

*The* reason to have market power is to be able to have access to the ability to profit from huge markups in constrained markets, because that's how you get your money before regulators notice.

The idea that this wasn't an obvious source of inflation is laughable, much as it was in December.