The Cantillon Effect and Credit Cards: The $257 Billion Payments Mess

The Cantillon Effect and Credit Cards: The $257 Billion Payments Mess

The Federal Reserve might be increasing or lowering interest rates for Wall Street, but it's the credit card cartel that structures interest rates for the rest of us.

Welcome to BIG, a newsletter on the politics of monopoly power. If you’d like to sign up to receive issues over email, you can do so here.

Today I’m writing about credit cards, and how the concentrated nature of the industry undermines business and monetary policy. Plus I’ll have some thoughts on Amazon’s purchase of One Medical and the retail giant’s recent acquisition spree.

In The Man Who Broke Capitalism, journalist David Gelles profiles how General Electric CEO Jack Welch transformed an icon of America from an industrial giant to a financial house of cards. Preferring to issue high-margin financial products instead of bending metal, Welch was at the forefront of the shift in the American economy towards banking and away from making things. And no other product symbolizes this shift more than the credit card, a business GE made its own in the 1990s, where the firm dominated the private label issuance market.

There’s a reason Welch went into this market in a big way. Credit cards are insanely profitable, roughly four and a half times more lucrative for the lender than any other form of credit. If you add up the two main streams of revenue, this industry generates up to $257 billion in revenue every year, which is about $780 for every man, woman and child. That’s a ridiculous amount of money for a payments system, far more than it should cost (and far more than it costs in almost every other country.) And as you’d expect, the reason for the excess profits is simple. Monopoly power and cheating. The American payments system is deeply concentrated, beset with unfair practices designed to sustain market power and hide true prices. As one industry consultant put it, financial institutions “hide the fees and the customers will still have to pay for them.”

Let’s start with the basics. Credit cards are two products combined into one. The first is access to a global payments network that lets a consumer and merchant transact. For consumers, a payments network seems free, but merchants must pay between 1.5-3.5% to middlemen on every single transaction, which amounts to between $61 billion to $137 billion a year. These swipe fees - which go to networks like VISA, Mastercard, or American Express, as well as issuing banks and processors - are essentially a private sales tax that goes to credit card networks and banks.

There’s very little competition in the payments system. VISA and Mastercard control 70% of this highly concentrated market. To give you a sense of the market power at work here, last year credit card networks raised their swipe fee prices to merchants by 24% and swipe fees are now the second highest cost for most businesses, after labor. In Europe, fees are much lower, because there’s a straight cap of 0.2% per transaction.

Where does this market power come from? Well merchants, even big ones, can’t afford to not accept Visa and Mastercard, so they have to accept whatever terms they are given. One key to this market power are credit card rewards, which are the points you get when you spend money through a certain card. These rewards are roughly $20 billion a year, mostly going to high-income customers and coming from the poor. According to the Boston Fed, “the lowest-income household ($20,000 or less annually) pays $21 and the highest-income household ($150,000 or more annually) receives $750 every year” as a result of these reward systems. Naturally, the credit card networks and banks keep most of the swipe fee money, but they pass enough of it back to cardholders to create switching costs in the form of customer loyalty. Almost everyone would be better off if swipe fees were lower than they are, but credit card users see a direct cash benefit, which ensures that they will continue using their cards, and that merchants will have to accept them.

The power these reward programs generate is then turned onto merchants, who aren’t even allowed foster competition between the big credit card networks. Visa, American Express and Mastercard have anti-steering provisions in their contracts with merchants, so merchants are not allowed to distinguish between different cards. That’s why you don’t see signs that say ‘use VISA and get a discount’ in local stores, even though VISA’s swipe fees are cheaper than American Express. Such a practice should be illegal, but it’s not. After years of legal wrangling, in 2018, the Supreme Court legalized this practice on procedural grounds, ensuring that this revenue stream would continue unabated.

The good news is there’s policy movement; Democratic Senator Dick Durbin and Republican Senator Roger Marshall just released a bill to address the problem by fostering more competition among credit card networks. And since every merchant in the country is angry about the excess fees they must pay, the politics here aren’t insurmountable.

BIG is a reader-supported newsletter focused on the politics of monopoly and finance. If you’re a paid subscriber, thank you! You make this work possible, and every comment, like, or forward of this newsletter is how we build this movement together.

If you are not yet a paid subscriber, please consider becoming one. BIG is journalism and advocacy that challenges power. You can always get lies for free. The truth costs a few bucks, but in the long run it’s much cheaper.

The second revenue stream for credit cards comes from credit products that allows a consumer to take out a short-term loan by carrying a monthly balance. Consumers pay interest and fees for the privilege, roughly $120 billion a year. Some of these charges include annual fees, fees for cash advances and balance transfers, rebates, minimum finance charges, over-the-limit fees, and late payment charges. Here too it’s quite lucrative. There’s about a trillion dollars in credit card debt outstanding, out of a total of $16 trillion in total household debt. While credit card defaults are higher than other forms of debt, total bank profitability in the U.S. was $279.1 billion in 2021. With $120 billion of revenue coming in just from interest payments and fees, you can see how good a business credit cards really are.

And yes, in the credit card issuance industry, there’s market power at work. Since 2005, there have been six firms who control roughly two thirds of total balances - JP Morgan Chase, Citibank, Bank of America, Capital One, Discover, and American Express. Since 2020, the Consumer Financial Protection Bureau has been examining whether there is real competition in the market, finding that the answer is, well, not really. From 2015 to 2019, “the average assessed interest rate on credit cards increased by more than 20% (from 13.7% to 16.9%).” And this was when the prime rate, which is linked to Federal Reserve policies, went up by just 2.25%.

There are a number of mechanisms credit card banks use to block competition and exploit consumers. First, some of the big banks withhold information to credit bureaus about borrower repayments, which makes it hard for competitors to offer better pricing to their customers. Second, it’s hard to actually get the price of credit card interest rates. You often have to apply to get that price, and that means you get a credit check, which reduces your credit score. Shopping across offers doesn’t make sense, so consumers look at rewards and annual fees, instead of interest rates. Third, it’s hard to refinance a credit card balance and switch cards. And fourth, credit card banks use a lot of fees, assessing $14 billion in late fee penalties alone in 2019, especially on people with worse credit.

On a more fundamental basis, credit cards are the mechanism by which most people receive their most flexible form of credit. I’ve written a good amount about the Cantillon Effect, which is the idea that a central bank, when it prints money and pushes it into the economy, ends up helping those with better political connections. In other words, money is not neutral, and the impacts of more or less money in a system are highly contingent upon the the set-up of financial institutions in that system. It came from an 18th century economist named Richard Cantillon, who pointed out that the people closest to a gold mine benefit the most from that gold mine.

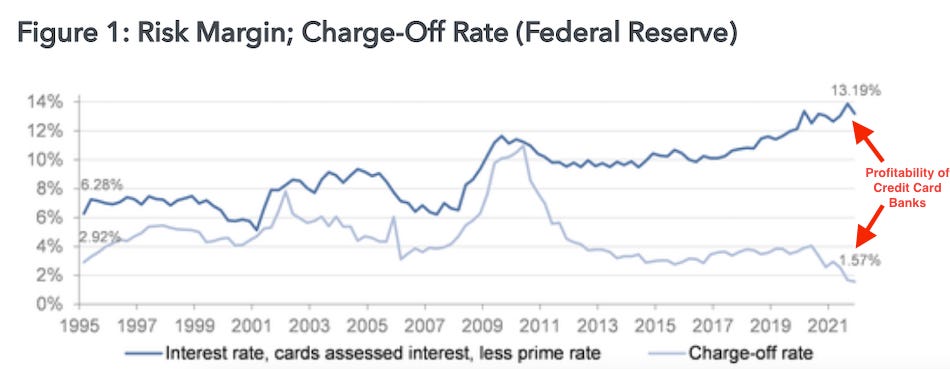

Today, the gold mine is the Federal Reserve, but too often economists don’t think about whether money is in fact neutral. They talk about how the Fed “lowers” and “raises” interest rates, but it’s not as if these changes occur equally across the economy. Wall Street is impacted immediately when the Fed lowers rates, and gets better borrowing terms. But credit card users, even though we assume their rates are tied to the general credit markets, do not. Because of the market power of the dominant credit card banks, their rates stay high no matter what. Their lenders will no doubt raise their rates when the Fed does, but there’s no reason to bring them down when the Fed cuts. It’s a one-way ratchet.

Indeed, if you look at the interest rate of credit cards vs other forms of consumer lending, what you’ll see is that credit cards are disconnected from broader changes in interest rates. The prime rate, which was roughly 9% in 2001, went down by two thirds, and yet credit card rates barely budged.

A little over a year ago, the White House issued an executive order on competition, encouraging agencies across government to attack monopolies and oligopolies in their sectors. The CFPB Director, Rohit Chopra, was well situated to implement this directive at his bureau, because he had just come from the Federal Trade Commission, which is an antitrust enforcement agency. And so he has already started, with the CFPB writing to six credit card banks asking for information about potential anti-competitive practices, as well as using its authorities to block junk fees by banks and consider ways to make it easier to switch credit cards.

These regulatory moves will take some time, but dealing with a bloated and politically connected industry doesn’t happen instantly. Credit card networks and banks are not only ripping us off and harming virtually every non-financial business in America, but they are even blocking the ability of the Federal Reserve to do monetary policy. And that’s not acceptable.

The Ridiculous Amazon-One Medical Deal

Amazon is on a buying spree, which is not a surprise considering the history of the firm going back to the mid-1990s. Of late it has purchased robot vacuum cleaner maker Roomba, and doctor clinic network One Medical, and is in the bidding for Signify Health, a home health care provider.

As one would expect, these deals are likely to result in a more concentrated marketplace, and we can see that happening already. Just a few weeks after buying One Medical, Amazon shut down its rival offering, Amazon Care.

Analysts said Amazon Care’s closure, which will come at the end of the year, should not be seen as a retreat on its efforts to gain a foothold in the $4tn US healthcare sector. “This is not a sign of failure by any means,” said Natalie Schibell at Forrester Research. “It’s a strategic move.”

Amazon’s decision comes after its recent agreement to acquire One Medical, a large network of primary care providers, for $3.9bn — its largest deal in the healthcare space. That takeover, if approved by regulators, would provide Amazon with much of the access to corporate employees it had been seeking with Amazon Care, said Christina Farr, health-tech investor at Omers Ventures, making the in-house platform redundant.

Companies such as Google offer One Medical to employees. “One Medical already has all these contracts, and does telemedicine,” Farr said. “It made sense for Amazon to acquire an existing network. Physician recruitment is really hard, building insurance contracts is really hard, building employer relationships is really hard. All of those things take a long time and One Medical was available to purchase.”

Both Amazon Care and One Medical sign deals with employers to provide health care to employees, so they are competitors. While neither Amazon Care nor One Medical has a particularly large market share, it’s clear that Amazon is foregoing internal investment in the hopes that it can buy its way into the health space. If the FTC blocks Amazon from buying One Medical, Amazon will simply build out its own doctor network, which would force it to compete to hire doctors.

This deal, in other words, is just about pulling a competitor out of the market and enabling Amazon to avoid having to invest in building its own services. That’s why this merger should be blocked, since it’s clearly reducing overall output in the market. It’s also astonishing that Amazon, while under investigation around the world, by Congress, and by the FTC, is entirely unchastened by any public scrutiny.

But then, these guys won’t believe that anything will happen to them, until something happens to them.

Thanks for reading. Send me tips on weird monopolies, stories I’ve missed, or comments by clicking on the title of this newsletter. And if you liked this issue of BIG, you can sign up here for more issues of BIG, a newsletter on how to restore fair commerce, innovation and democracy. If you really liked it, read my book, Goliath: The 100-Year War Between Monopoly Power and Democracy.

cheers,

Matt

US banks don't compete for customers on interest rates.. they compete for them with rewards. With the right incentives, consumers are willing to look past the APR line.

The only reason the card networks charge their interchange fees isn't really for the networks themselves.. its so they can pass it to the banks who then decide what to keep and what to kickback to the customer. The European fee caps (and the US regulatory caps on debit card fees) are proof that these payment networks can run on much less. The credit card industry is a payment system that sucks out money through obfuscation. The rewards system creates a moat for the existing networks/banks against a competitive system. Consumers won't go to an alternative system unless the rewards are better. Better rewards means charging higher interchange which the merchants won't sign up for. I think the anti-steering provisions that Matt mentions are highly anti-competitive.

Biden's student loan bailout is a big victory for credit card issuers. The obvious answer to student loan debt is to make it like medical and credit card debt to be dischargeable in bankruptcy. However, this would have millions filing for bankruptcy and they would not only be able to write off student loan debt, but credit card debt as well.