The Cantillon Effect: How the Federal Reserve Caused a Massive Merger Wave

The Cantillon Effect: How the Federal Reserve Caused a Massive Merger Wave

How Fed Chair Jay Powell undermines antitrust enforcement.

Welcome to BIG, a newsletter on the politics of monopoly power. If you’d like to sign up to receive issues over email, you can do so here.

In March of 2020, Congress and the Federal Reserve coordinated in joint actions to backstop the financial markets, which were going haywire because of the pandemic. This was encapsulated in the CARES Act, which legitimized the endless bailouts from the Fed towards private equity and the corporate sector.

At the time, I called it a ‘corporate coup,’ explaining through what is known as the Cantillon Effect that money printing as it was done would lead to significant corporate consolidation. And so it has. The Wall Street Journal reported that after only 8 months, 2021 is the biggest year for M&A since they started keeping records. One McKinsey consultant recently put it, “When you’ve got the Fed saying debt will stay cheap for years, plus historically high multiples, the numbers look buoyant — especially if you’re a seller.”

This was all predictable. In April of 2020, my organization plus a number of nonprofits warned about the problem, sending a letter to Fed Chair Jay Powell asking the central bank to put restrictions on monetary actions to stem massive consolidations. Multiple members of Congress, led by Elizabeth Warren, tried to put a temporary merger prohibition into the various pieces of legislation then wending their way through Congress.

Powell, unfortunately, ignored the warnings he was receiving, and Congress didn’t enact a merger prohibition. Noah Phillips, the Republican FTC Commissioner who opposed Trump’s antitrust suit against Facebook, attacked the idea of a merger ban, saying that the FTC was not overwhelmed with merger filings. “There is no evidence of a merger “wave”, or that the [FTC] is overwhelmed with HSR filings,” he wrote on a well-known libertarian blog. Of course, the signs of a coming wave were obvious, but Phillips didn’t want to see them.

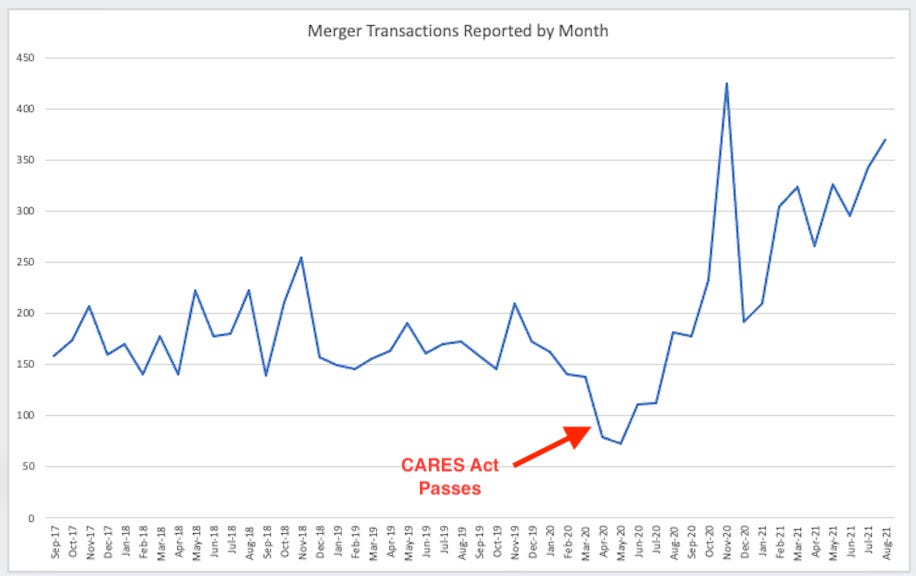

Flush with cheap government backstopped capital and little resistance from antitrust enforcers, Wall Street went crazy with mergers. Here’s a chart I put together using Hart-Scott-Rodino data from the Federal Trade Commission, a law that requires firms to report mergers over a certain size.

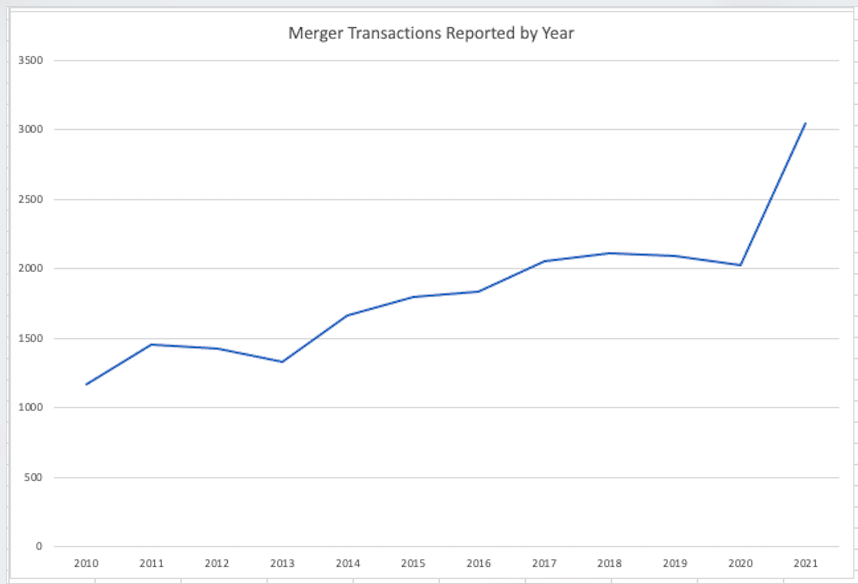

Already the number of mergers in the first eight months of this year has far surpassed the total number for all of last year. Here’s an annual chart, with a projection of the total number of mergers for 2021 based on the current pace of transactions reported.

And this gets to the administrative problem at the agencies. Antitrust officials have 30 days to evaluate whether a merger should be investigated, and then they can ask follow-up questions. If they still want to investigate, they get a few more months to challenge the merger, which means putting together large, complex commercial litigation in a very short amount of time. If they don’t, the firms will go ahead and combine operations.

As the burden to prove a merger is problematic increases due to monopoly friendly judges, the workload has gone up over time to stop any particular merger. It’s not impossible to stop them. In July, the Department of Justice stopped insurance giants Aon PLC and Willis Towers Watson from combining. But each one takes a staff going through millions of documents, even when the merger is obviously illegal. And as the number of filings goes up, and the agencies begin going after big tech through suits against Google and Facebook, the workload becomes crushing. To put it differently, the workload of the agencies has gone up by 50% since the CARES Act passed and Jay Powell subsidized a merger wave.

A simple fix would be to tweak the merger process and let U.S. enforcers operate like European agencies, which is to say allow them to stop firms from combining operations until they are cleared to do so. There are many other possible fixes, like legislating rules that block mergers above a certain size, or stopping mergers when there are fewer than five firms in a market. But right now, the antitrust enforcers aren’t just trying to stop mergers, they are also fighting the Fed’s cheap money policies and lax regulatory choices encouraging such combinations. Congress should pay some attention.

Matt, you must be channeling the hard-money, gold-bug right, people like Jim Grant and Bill Fleckenstein. They've been saying stuff like this about the Fed for more than 20 years. I first learned about the Cantillon effect from reading Murray Rothbard, Mr. Anarcho-Right, "denationalize money" himself from decades ago. Rothbard was the main thinker responsible for the introduction of the Austrian School into economics in the US, apart from Hayek, who became well-known for The Road to Serfdom on his own.

Earlier this year, the Grant's Interest Rate Observer podcast did an amazing interview with Karen Petrou, who published book last year about how much our economy and society have been distorted by the Greenspan-Bernanke-Yellen-Powell era in Fed policy. You should interview her. An urgent necessity: an end to QE and a return to moderate positive real rates. This is the 2021 equivalent of what Volcker did with inflation in 1980-83. It will be painful, because the problem is deeper, longer-lasting, and more insidious than in the late 1970s.

The master book from this point of view, apart from Grant's books, is The Great Deformation by David Stockman, a reformed ex-private equity shark and Reagan's one-time budget director. His diagnosis runs much earlier, back to the Populist era and the rise of "flexible money," which eventually became captured by the Washington-Wall Street alliance. He talks quite a bit about the distortions in M&A and other consolidations driven by a long era of negative real interest rates and unlimited free credit at zero nominal rates.

All these asset markets go nuts under these conditions for the simple reason that there's no longer any check on the credit creation machine that benefits a narrow, self-serving class (which includes many political figures in DC) -- no gold standard, no reserve ratios, no Glass-Steagall Act.

Until then, I shall continue to tease you about your ill-disguised hard-money, gold-bug right-leaning tendencies when it comes to the Fed. These are *real* libertarians BTW, not neoliberals. Keep that distinction in mind ;-)

Nice Austrian take here.