The Fed Can't Print Semiconductors

The Fed Can't Print Semiconductors

Influential D.C. operator Jay Powell admits that antitrust might be key to bringing down prices. Certainly solving the semiconductor shortage is.

Welcome to BIG, a newsletter on the politics of monopoly power. If you’d like to sign up to receive issues over email, you can do so here.

A few weeks ago, Fed Chair Jay Powell testified for his renomination hearing, and with inflation at a scorching 6.8% and the Federal Reserve as the only major government institution trusted by the political class, he himself is in the hot seat. Powell is an insanely smooth D.C. powerbroker, having been an important lawyer, Treasury official, and private equity baron, sitting at the nexus of big money and big government for much of his life. What’s interesting about Powell though is that he’s not an economist, and he doesn’t see the world through models. He’s quite respected by economists, but he isn’t one himself. His main experience professionally is investing and corporate work, as well as the dirty politics of helping banks navigate the government.

Inflation is a highly political subject, and the Democrats are trying to find a way to pin the problem on large firms. At the time of the hearing, a lot of people focused on the semi-hostile back-and-forth with Elizabeth Warren, wherein she kind of forced him to admit that inflation could be driven by market power. On Wall Street, this was sort of dismissed, as the ‘oh well you know that annoying Senator Warren.’ But what’s interesting is that at a couple of other moments in the hearing, Powell volunteered in a much more low key way something similar to what he said to Warren.

The dynamic in inflation is figuring out how much of the increase in prices is coming from consumers having more cash and borrowing power they are using to spend, and how much is coming from producers having a hard time making what people want to buy. Most economists think the problem is related to too much cash in the hands of consumers. But Powell actually argued, at one point to Senator Chris Van Hollen that “a big part of getting inflation back down” is getting “significant relief on the supply side so that global supply chains loosen up,” meaning “more semiconductors so that we can start manufacturing cars again.” The semiconductor shortage, which Paul Krugman called a ‘random event’ in a debate with Larry Summers, is one of the more difficult policy problems we have, intertwined as it is with antitrust, industrial policy, trade, and finance going back 40 years.

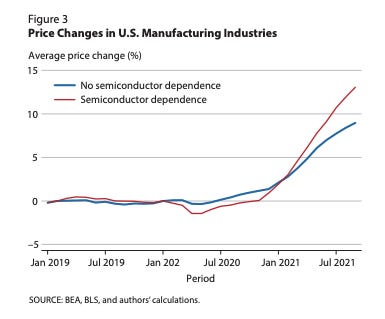

There isn’t much research on the relationship of semiconductors and inflation, but one paper that came out recently from the St. Louis Fed suggests that semiconductors matter, a lot. The paper measured pricing changes in the “170 manufacturing industries that do not use semiconductors as a direct input and the remaining 56 manufacturing industries that do,” finding that dependent industries hiked prices by 40% more than non-dependent ones.

The paper understates the pricing pressure, because even industries that don’t use semiconductors as direct inputs rely on semiconductors. For instance, everyone relies on trucking, and truckers can’t repair their trucks because of a lack of semiconductors that go into certain parts. Powell knows this, and admitted it. He also knows how bad things are at the ports. In response to a question from Richard Shelby, he explained that the Fed’s failure to predict inflationary increases was in large part a result of them not understanding that the supply side problems wouldn’t get fixed.

So on inflation, why did we say transitory? We said that because we thought that the supply side bottlenecks and shortages would be alleviated much more quickly than they have been. There's no empirical experience with this before, we haven't had the global supply chain collapse. We haven't had this kind of a labor force shock before so we and essentially all other mainstream forecasters forecasted that by now we'd be seeing much lower inflation.

And that's not what happened. So what's changed is that just as I mentioned, the supply side constraints have been very persistent and very durable. We're not seeing really a lot of progress. If you look across you know, the global supply chains and what's happening domestically, look at our ports.

Look at Long Beach in LA, the two big ports on the west coast for Asia, the number of ships at anchor is still at a record level. So we're not really seeing yet the kind of progress we essentially all forecasters really thought we'd be seeing by now and that's that's really what's driving it. I think we did foresee the strong spike in demand. We didn't know that it would that it would be so focused on on goods but that's really what happened.

And I think we learned that it wasn't that it was just it. This is a unique set of circumstances we thought really the United States economy is so dynamic, the supply side would adapt quickly. And you know there are new companies being started and old companies dying all the time. This is a situation where there actually are hard constraints.

People want to buy cars, car makers can’t make any more cars because there are no semiconductors. So that's never happened. I can't think of another example of that.

At another point, Powell went back and forth with Senator Mike Rounds of South Dakota on cars, inflation, and meat prices, and consistently noted how much of the problem was outside the powers of the Federal Reserve and in the hands of competition policymakers. Rounds comes from a state where “cows outnumber people,” but ranchers, he told Powell, aren’t seeing price increases at the farm gate, even as consumers are having to pay a lot more for beef. So how much inflation, he asked Powell is coming from supply vs demand. Powell said he couldn’t say.

And that right there is the state of the Fed’s best macro-forecasting. They just don’t know. If only economists would be a bit more humble about the problem.

Here’s Powell’s back and forth with Rounds.

Sen. Mike Rounds (R-S.D.): The consumer price index rose 6.8% In November, there appears to be consistency on that line. Part of that you have the opportunity to impact with regard to the demand side. Can you talk to us about your discussions or at least your analysis of how much of the inflationary trends we're seeing you have the ability to impact with your monetary policy?

Jerome Powell: We don't have much ability to affect the supply side. And if you look at where the really big contributors are to the overshoot from inflation, it's in the good sector still, largely and that's cars that's new, used, and rental cars, it's appliances.

Sen. Mike Rounds (R-S.D.): What about food? Hamburger at over $5 a pound?

Jerome Powell: Yeah, no, that's see that's not something we can't. I'd say that there are supply side issues there too, as you and I have discussed, but those are really outside the range of our of our tools.

Sen. Mike Rounds (R-S.D.) Is it fair to say petroleum products as well, the price of gas over $5 a gallon. Those are items that are supply side. They're not the demand side. The supply side of this is a significant part of the entire inflationary demand. Fair to say that your focus is on the demand side, not the supply side, correct?

Jerome Powell: That is right.

Sen. Mike Rounds (R-S.D.): What percent of that inflationary trend are you trying to impact with the demand side monetary policy that you have the ability to impact?

Jerome Powell: It'd be hard to break it down in that way. I would say it this way, though. Right now our policy is very highly accommodative. So we're stimulating. We're not restraining demand at all. At this point.

Sen. Mike Rounds (R-S.D.): But it's not political in nature. It is economic in nature to say that inflationary trends that we are seeing are partially from the ability of consumers with cash in their pockets to be able to pay a higher price. But second of all, is because of the limitations and the bottlenecks that we find within the supply side of our economy, correct? Yes.

So let's just take food as an example. I come from South Dakota where cows outnumber people, and yet we have producers there. Are there on a regular basis talk about the fact that they don't see an increase in what they're receiving for livestock. And yet our consumers across the entire country are seeing huge increases in the price of meat and in between them.

Four packers who control over 80% of the market showing record high profits, while consumers pay huge inflated prices. That's something which has to be dealt with with policy, and not necessarily something that the Fed can impact. Correct?

Jerome Powell: That's really a competition policy question.

Just a few decades ago the tech companies were run by engineers, in partnership with the financial people. There was this constant battle between the two where the engineers wanted to create cool products and the financial people wanted to be profitable.

And that tension worked. You needed the financial focus on profits to stay in business. And you needed the engineering focus on products to create brilliant new products. One of the best examples of this is Disney that was lead by Walt AND Roy Disney. Both were necessary for their success.

So what happened? Not only did the financial people gain sole control, but their focus shifted from being profitable to their stock price. This was a giant shift.

If you want to solve this issue, you need to find a way to revert back to how these companies used to be managed. Key to that I think is remove this absolute hold Wall St has on the boards and C suite of the companies.

And part of that is different people with very different priorities and value systems, on the boards and in the C suite.

So a question on the port issue. If most of these carriers are international,do we have a feel for why a port live Vancouver is being underutilized ? I’ve seen this before. Why not now ? Or is it ?