The Price-Fixing Economy

The Price-Fixing Economy

New information coming to light in Amazon and meat price-fixing antitrust cases shows inflation is probably being driven by consolidation in the form of data sharing.

Welcome to BIG, a newsletter on the politics of monopoly power. If you’d like to sign up to receive issues over email, you can do so here.

Today, the government came out with a ‘blowout’ report showing massive growth in the number of jobs in the economy. Among normal people, polling on the economy is still abysmal, even though the numbers suggest they shouldn’t be.

Among elites, the reaction to this report is that, believe it or not, things are too good for normal people. Stocks are dropping, because Wall Street thinks that the Federal Reserve will likely tighten financial conditions, as policymakers still believe - despite much evidence to the contrary over the last three years - that inflation is caused by workers getting too much money.

In this piece, I’m going to show how recent antitrust suits undercut this theory, and also suggest an additional reason why the public is unhappy with the economy. It’s not just that prices are high, it’s that they are increasingly unfair.

Whither Greedflation?

For roughly a year after the pandemic, populist thinkers and writers posited the theory of ‘greedflation’ to describe why prices were skyrocketing. They noted that CEOs were constantly noting on investor calls that they had pricing power or their industry overall had ‘disciplined’ its capacity. One CEO, for instance, said publicly he was “praying for inflation” so he could raise prices. I added something to this argument in late 2021 when I noted that higher corporate profits explained roughly 60% of the inflationary increase. Eventually, scholars and Federal Reserve officials began releasing data confirming this thesis.

But status quo oriented economists quickly intervened, and mocked the theory into the ground. "My friend and economist Jason Furman says, 'Blaming inflation on greed is like blaming a plane crash on gravity,'" said economist Justin Wolfers in November of 2022. "It is technically correct, but it entirely misses the point." MIT economist David Autor made a simple point to discredit the idea. “Market concentration is a longstanding problem, yet we’ve had close to no inflation for two decades,” he said, “so it cannot be that market concentration suddenly explains inflation.” And then of course, there was Larry Summers.

A couple of antitrust cases over the last month are suggesting that concentration may have played a more significant role than commonly understood, but we just don’t have the data to measure it. Two weeks ago, the Antitrust Division filed a complaint against a firm called Agri Stats, which sells data and consulting services to the processors that dominate the poultry, pork, and turkey industry.

The claim in the case is that Agri Stats was a coordinator of pricing, serving as a clearinghouse where it would collect and share granular pricing, wage and production data for all major meatpackers. Agri Stats also sold consulting services, which one executive at Smithfield, a pork processor, summarized with four words: “Just raise your price.”

The poultry, pork, and turkey industries aren’t technically monopolies, as there are multiple firms who sell these products. But Agri Stats, by making sure everyone in the industry colludes, applied a form of unified control of pricing to the industry. It’s multiple firms, but in one centralized cartel.

There are several key questions here. One is whether this kind of collusion is systemic across the economy. I suspect it is. After all, Agri Stats wasn’t hiding its business. This is what it has on its website, marketing material that is pretty close to ‘we sell price-fixing conspiracies.’

But are there other examples? Yes. One mind-blowing story from ProPublica that came out in 2022 was about landlord software sold by a firm called RealPage, which essentially told big landlords to raise rents by showing them “data RealPage gathers from clients, including private information on what nearby competitors charge.” There’s a quasi-consulting arrangement here too, as “RealPage discourages bargaining with renters and has even recommended that landlords in some cases accept a lower occupancy rate in order to raise rents and make more money.”

RealPage is now facing at least seven private antitrust class action suits, as lower output and higher prices are classic signs of monopoly power. What’s fascinating is that here again, an economist would look at these markets and see competition and multiple rivals renting out apartments, but they would miss that there’s a cartel, or rather a set of regional cartels coordinated by a software platform, operating to boost prices and margins.

Sometimes the price-fixing is done through software and data exchange, and sometimes it’s done through signaling in concentrated markets. In its recently filed complaint against Amazon, for instance, the Federal Trade Commission touched on something called Project Nessie, an internal algorithm “to test how much it could raise prices in a way that competitors would follow.” Amazon would raise a price to see if competitors followed, and then keep the price high if they did, or drop it back down if they didn’t.

Basically, Amazon wasn’t just hiking its own prices, it was signaling to rivals that they should hike their prices as well. I spoke with a former Amazon retail division official, who told me about how much they hated Project Nessie internally, because it was a collusive mechanism imposed upon the retail division which drove up prices to consumers.

From a legal perspective, it’s interesting the Federal Trade Commission didn’t make a monopolization claim on Project Nessie, but an argument that this kind of algorithmic collusion is what is known as an unfair method of competition, which is a more expansive claim that allows for a looser market definition. In certain areas, like selling expensive cameras, people do comparison-shop. But even though there is competition, Amazon has market power, and Project Nessie is an unfair exploitation of that market power to drive up prices everywhere. It’s a cartel done via algorithm.

BIG is a reader-supported newsletter focused on the politics of monopoly and finance. If you haven't done so already, please consider supporting this work by upgrading to a paid subscription. The truth costs a few bucks, but in the long run it’s much cheaper.

I suspect these forms of coordination are far more common than we assume. You might think the restaurant industry is competitive, and it is. But the payment software for restaurants is much less so, and when consumers are presented with a bill at a restaurant, the screen regularly offers not the traditional 15% tip, but the choice of tipping 20%, 22%, or 25%. Is that collusion? No. But’s a loosely coordinated form of a price hike to allow firms to pay employees less than they would ordinarily have to. And tipping is now being baked into all sorts of firms, from juice shops to appliance-repair firms to plant stores to locksmiths. 16% of small businesses now ask customers to leave a tip, up from 6% in 2019. Again, this change is almost certainly a shift in the software firms use to accept payments, and it’s a price hike and form of coordination you won’t see in concentration statistics.

That said, even if you think forms of price fixing are systemic, there’s another important question. Did this kind of coordination increase during the pandemic and drive inflation? And there, the answer is we just don’t know. Project Nessie ended in 2019, when the House Antitrust Subcommittee began investigating Amazon. Agri Stats changed some of its practices in 2019 as well, after there were class action suit filings. I find it hard to believe Amazon and meatpackers aren’t continuing these practices in some form or fashion. Moreover, competition is cumulative, and so is collusion. If a bunch of firms have collectively held back on supply for years, they can’t suddenly build a bunch of factories to expand production. In other words, if an industry is historically concentrated, collusive and genteel, then prices won’t move very much for a while, even if formal agreements stop.

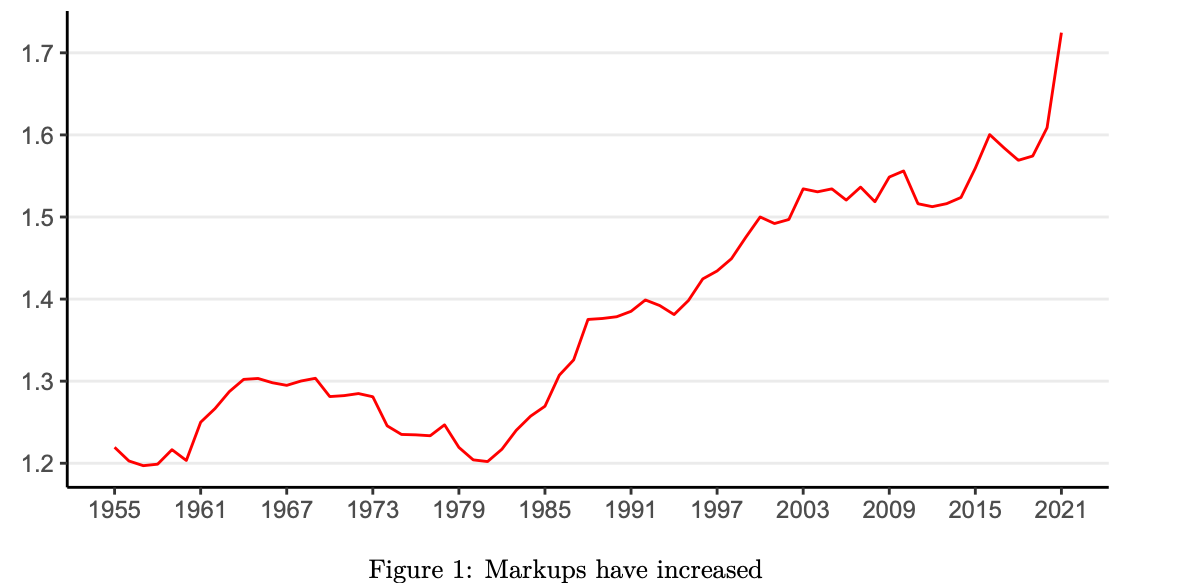

Indeed, Mike Konczal and Niko Lusiani, in a paper titled “Prices, Profits, and Power,” showed how markups exploded during the pandemic, and that the increases in 2021 were “both the highest level on record and the largest one-year increase—over 2.5 times the increase of the next several largest annual increases.” Was that a function of more single firms operating as monopolies, or more concentrated industries colluding to act as cartels? The answer is likely, yes.

More broadly, price-fixing isn’t always about driving prices up, it can also be about driving wages and supplier prices down. Meat processors weren’t just colluding in jacking up prices to consumers, but lowering wages to workers. And in a non-inflationary environment, prior to 2021, it was easier to reduce prices to suppliers than increase prices on consumers. Indeed, the decade of the 2010s was one in which there was remarkably slow wage growth, which is consistent with a story of heavy concentration on the labor side (which economists have now realized is pervasive.)

It was only when there was a broad narrative shift towards inflation that businesses began increasing prices dramatically, and that’s when price-fixing turns from pressing down prices from workers and sellers and towards raising prices on consumers. It isn’t ironclad that profits drove inflation, but these cases do suggest that statistics about concentration are at best incomplete.

Fair Prices, Not Just Low Prices

One of the core political dynamics in American politics is that our economic and political elites see the world almost entirely differently than normal people, and there’s no better case study for this than inflation. It’s something I’ve written about extensively - why do Americans think inflation is up and the economy is bad when all the dials and data policymakers use show that these are boom times?

I’ve answered part of this question by showing that the dials themselves are broken, that the cost of interest charges isn’t included in inflation metrics. But I also have a suspicion that the increase of tips and junk fees - which are exploding in usage by businesses - is causing people to say inflation is too high, not just because everything is so costly but because the prices are also unfair.

Buying a ticket to a game or concert and seeing a crazy fee, or being presented with a tip screen for a locksmith and having to choose between social awkwardness and paying a higher price, feels crappy. Being cheated is not only frustrating, it’s also scary, because it can recur without warning and cause unexpected costs. Being cheated thus imposes a real extra cost beyond the amount someone has to pay, which is to say, increasing uncertainty about future prices.

So this is another part of the answer about why sentiments on the economy are negative despite evidence of less inflation and more jobs. Pollsters are asking about inflation by framing it in terms that economists understand, which is to say the level or the rate of increase. But ordinary people not only want to pay good prices, they also want to feel like they are being treated fairly. If people feel increasingly cheated, and the only questions they are asked by pollsters are whether the economy is good or whether inflation is up, they will give an answer that reflects their anger and fear of being taken advantage of, and not reflect the ‘objective’ statistics policymakers expect.

This too is not a new problem. For thousands of years, political philosophers have wrestled with the problem of the ‘just price’ for goods, and every society regulated prices to get close to fairness. Indeed, the Federal Trade Commission, and many other areas of government, have statutes that bar “unfair” methods of competition or “unfair” consumer pricing practices, because fairness, not just the level, is something that makes a society function. These kinds of laws seem quaint today, and antitrust lawyers and economists regularly mock the very concept of fairness. But by airbrushing out the human element of commerce, and narrowing the only moral question to efficiency and price level, economists have destroyed the ability of policymakers to see commerce and understand the economy the way the rest of us do.

Thanks for reading! Your tips make this newsletter what it is, so please send me tips on weird monopolies, stories I’ve missed, or other thoughts. And if you liked this issue of BIG, you can sign up here for more issues, a newsletter on how to restore fair commerce, innovation, and democracy. And consider becoming a paying subscriber to support this work, or if you are a paying subscriber, giving a gift subscription to a friend, colleague, or family member.

cheers,

Matt Stoller

Indeed, the sense that as consumers we feel we are being treated unfairly is a powerful emotion that overcomes all of the data that point to a robust and growing economy. Keep up the good work. I love your newsletter.

There is an important distinction here. Monopoly power is not inherently inflationary. The theory is better framed as arguing that monopoly power serves as a dangerous amplifier of monetary conditions--accelerating deflation through input and labor pricing power during economic contractions and then accelerating inflation during times of economic expansion via raising prices. Arguing monopoly power is inherently inflationary is a weaker position than arguing it is a destabilizing force in either cycle. This framing makes intuitive sense, as competition is what brings a free market economy into equilibrium. Monopolies create disequilibrium.