Reversing Reagan: Is Wall Street Giving Up on Consolidation?

Reversing Reagan: Is Wall Street Giving Up on Consolidation?

Following Illumina's loss, Adobe throws in the towel in its merger attempt with Figma. Meanwhile CNBC's Jim Cramer chides the antitrust defense bar and agencies release merger guidelines.

Welcome to BIG, a newsletter on the politics of monopoly power. If you’d like to sign up to receive issues over email, you can do so here.

Are CEO’s finally getting the message? Today one of the premier deals on Wall Street fell apart, as design software monopolist Adobe abandoned its $20 billion attempt to buy nascent rival Figma in response to pressure from the Antitrust Division and European enforcers. This is on top of legal losses by corporate giants last week, and another hospital merger abandonment today.

Meanwhile, CNBC’s Jim Cramer chided antitrust defense lawyers for misleading corporate executives on what kind of mergers can get through the regulatory gauntlet. And all of this is happening the day that antitrust agencies released new merger guidelines designed to restore antitrust law to what Congress intended.

Every Sunday, I do a round-up of monopoly news for paid subscribers. Yesterday’s was titled “We're Slowly Breaking the Will of the Bad Guys,” and was about a number of victories by enforcers over the past week, spearheaded by the Google antitrust loss in a jury trial, the Federal Trade Commission’s win over pharma giant Sanofi’s tie-up with a Maze line of business, as well as an appeals court win blocking genetic sequencing machine monopolist Illumina from buying cancer test producer Grail.

Today came two other wins. First, design software producer Adobe gave up on its acquisition of rival Figma due to a realization that they were unlikely to convince regulators that the deal was legal. This was huge, front-page news because the deal was one of the biggest Wall Street mergers of the year. Adobe was facing the Antitrust Division in the U.S., led by an aggressive lawyer named Jonathan Kanter, as well as the E.U. and the U.K. Here’s Figma CEO Dylan Field:

Second, the FTC and California Attorney General Rob Bonta announced they blocked the merger of a hospital system in Northern California, as John Muir gave up on its takeover of San Ramon Regional Medical Center from Tenet Healthcare. This merger would have increased prices for services such as heart surgery, spinal surgery, and maternity care in the area. American health care is a nightmare of high prices, and the reason is a policy regime that prioritizes consolidation. Stopping one-off hospital mergers isn’t enough, but it’s something.

The Adobe loss is a critical signal to deal-makers, as the design software firm decided to pay a $1 billion break-up fee rather than fight in court to get its merger approved. A big merger is not easy to pull off, requiring the coordination of a whole bunch of highly intelligent and risk-averse lawyers and bankers across a number of different institutions. They become impossible quickly when everyone is terrified they’ll get personally thrown under the bus by other sharks.

When Illumina lost, its CEO, Francis deSouza, paid the price with his job; activist investor Carl Icahn is even trying to hold the board members who did the deal personally liable. Getting in trouble over a deal is not actually uncommon. Every merger has big winners and losers, and there are risks at every level, with significant breakup fees, board member liability, and financing uncertainty, as well as post-merger legacy embarrassment.

The actual end of the Adobe-Figma deal is a good thing. Both firms will go their separate ways, competing to bring the best design software integrated with AI image generation. Tight merger control is a form of industrial policy to prioritize production over finance. For instance, in contrast to the Figma CEO, there’s Jordan Singer, who builds artificial intelligence technologies at the firm, who was quite optimistic, tweeting after the deal fell apart, “I can’t wait for you to see all the things we’ve been working on. It’s gonna change everything.” It’ll be a fascinating market dynamic to watch, seeing if competition is better than allowing a firm like Adobe to continue rolling up the market.

The merger world isn’t dead, of course, with Nippon Steel announcing an acquisition of U.S. Steel for $14 billion. I’m not sure there’s much of a competition concern with this tie-up, but even that one will require review by the United States Committee on Foreign Investment, which screens for national security issues. Already, the United Steelworkers union is screaming bloody murder. So even deals that wouldn’t ordinarily cause problems are now more difficult for everyone involved.

Reversing Reagan

In April of last year, I wrote up what created our deeply unfair and increasingly authoritarian economic order, a successful conspiracy by antitrust lawyers and economists in the early 1980s to rewrite merger law without going through Congress. This plot was accomplished through lobbying by Reagan Antitrust Division chief Bill Baxter to end private enforcement of antitrust, as well as, most importantly, Baxter’s rewrite of merger guidelines in 1982. Here’s the chart of a merger explosion that started that year, and never stopped.

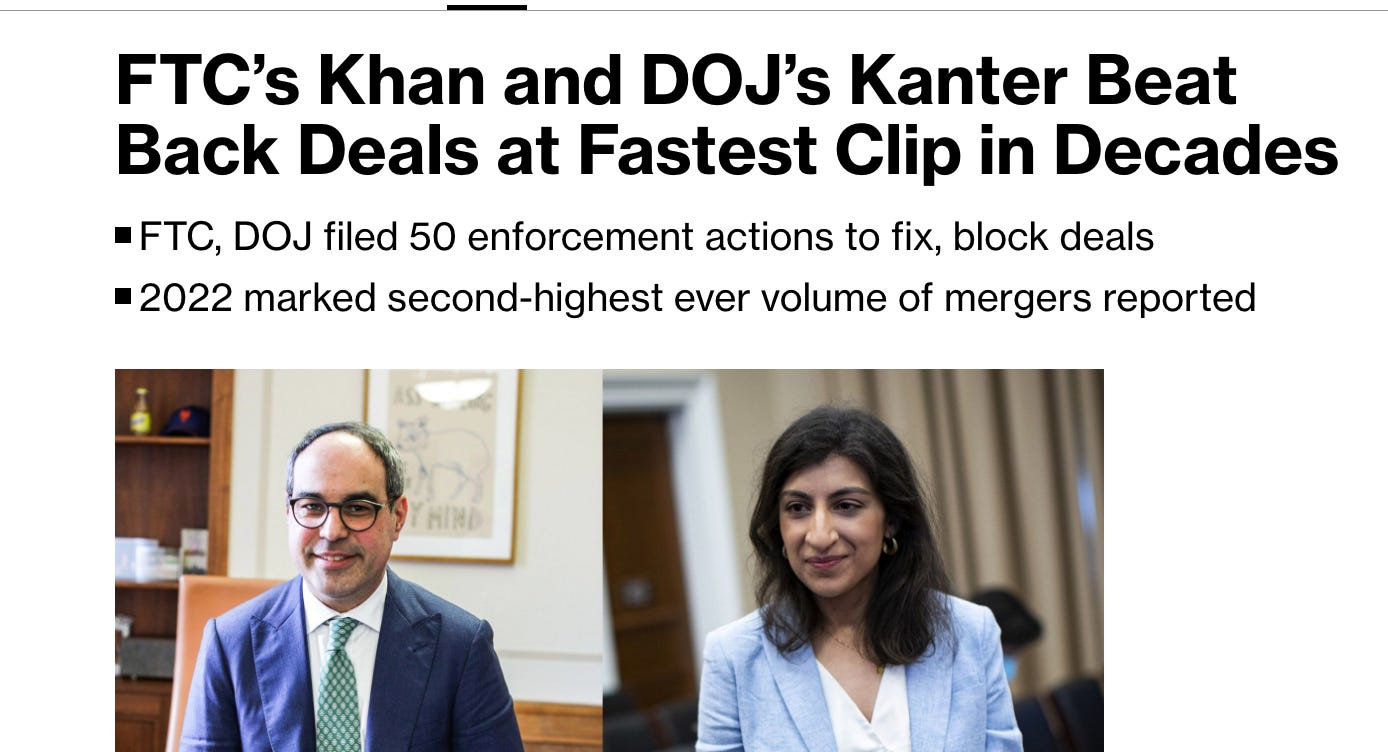

Baxter’s project is what FTC Chair Lina Khan and Antitrust Division chief Jonathan Kanter sought to end. And today at noon, Antitrust Division and the Federal Trade Commission released new merger guidelines, the critical guidebook on how enforcers think about merger enforcement. If the legal actions represent a new way of thinking, these guidelines are the codification of that new thinking.

There’s a bunch of interesting slight changes in these new guidelines, such as inclusion of pricing algorithms and multiple citations of the Fifth Circuit Court Illumina decision from Friday. But mostly it’s an announcement that the era of permissive antitrust is over. (These guidelines have been in the works for years, and many of you submitted public comments, which the agencies took quite seriously.)

None of this is going unnoticed on Wall Street, of course, who have waged a remarkable and effective campaign to demonize and belittle enforcers. That’s why, if you talk to your friends, they probably haven’t heard of any of the actions by anti-monopoly enforcers. This campaign to undermine or downplay the public perception of antitrust is spearheaded by the Wall Street Journal editorial page, corporate lawyers, men like former Obama advisor Larry Summers, and pundits such as Jim Cramer on CNBC, who today called Khan a ‘one woman-wrecking crew’ for stock portfolios.

Here’s Summers in July on the draft merger guidelines.

But perhaps more pernicious than the actively hostile are the neutral journalists who quote from bought and paid professors, lawyers, and economists, some of whom have top-tier credentials, like this Stanford economist who got $3 million from Google for expert witness work. There are some great examples of this kind of writing over the last month.

Early last week, former corporate lawyer Ankush Khardori wrote a New York Magazine piece titled “Lina Khan’s Rough Year,” citing multiple anonymous big tech attorneys about her supposed managerial incompetence, and highlighting FTC court losses. Similarly, two former state attorneys general turned big tech advisors argued in Fortune that Lina Khan is losing in court and doing things all wrong. And a business school professor who nicknames himself the ‘CEO whisperer’ - Jeff Sonenfeld - went after Khan for “destroying American competitiveness” and, well, yes, being a loser.

Khardori’s piece was cited widely, which is important, because he did not mention, say, Google’s antitrust liability, or any other anti-monopoly accomplishment. Nor could the major court victory of the Fifth Circuit make it into the piece, or any update. So readers take away that this is yet another area where there’s big talk and little action, even though that’s not true.

Nevertheless, I noticed something new today. Wall Street is getting more cautious after this series of enforcement wins, and the Fifth Circuit Illumina decision ratifying them. This morning, Cramer, while criticizing Khan, also attacked corporate lawyers and deal bankers for giving bad advice to CEOs, telling them they can get deals done when in fact they can’t. Cramer plays an over-the-top character on TV, but even he can’t keep up the charade with his executive friends that deals are gonna get through. And now he’s telling on the antitrust priesthood for misleading his buddies.

Now, this more cautious posture is anything but permanent, as a judge has yet to rule on JetBlue-Spirit, and deal-makers could get a green light if there’s a new President in 2025. But Wall Street dealmakers and lawyers are the most irrationally confident people I’ve ever met, and they are now voicing public doubts about consolidation.

That’s new. And just in time for Christmas.

Thanks for reading. Send me tips on weird monopolies, stories I’ve missed, or comments by clicking on the title of this newsletter. And if you liked this issue of BIG, you can sign up here for more issues of BIG, a newsletter on how to restore fair commerce, innovation and democracy. If you really liked it, read my book, Goliath: The 100-Year War Between Monopoly Power and Democracy.

cheers,

Matt Stoller

Love it Matt. Thanks for your great work. Merry Christmas.

The important thing is to keep up the antitrust momentum. If it stalls then a long time could pass before there is another opportunity to reign in monopolies.